Thilo Wallenstein

Partner - Munich

In our EMEA supply chain survey, we discussed how companies have reordered sourcing priorities, with efforts now aimed at diversifying supply bases and employing near- or onshoring strategies.

Here, we take a deep dive into the implications for the DACH region (Germany, Austria, and Switzerland), revealing the reality check required regarding decreasing dependence on China, plus examples of government incentives in place across a number of sectors.

Our key findings

Strategic implications for executives

Sourcing alternatives is key for DACH companies:

Comparable to other EMEA companies, Make vs Buy strategies and government incentive programs remain important to DACH businesses:

Decreasing dependence on China: A reality check

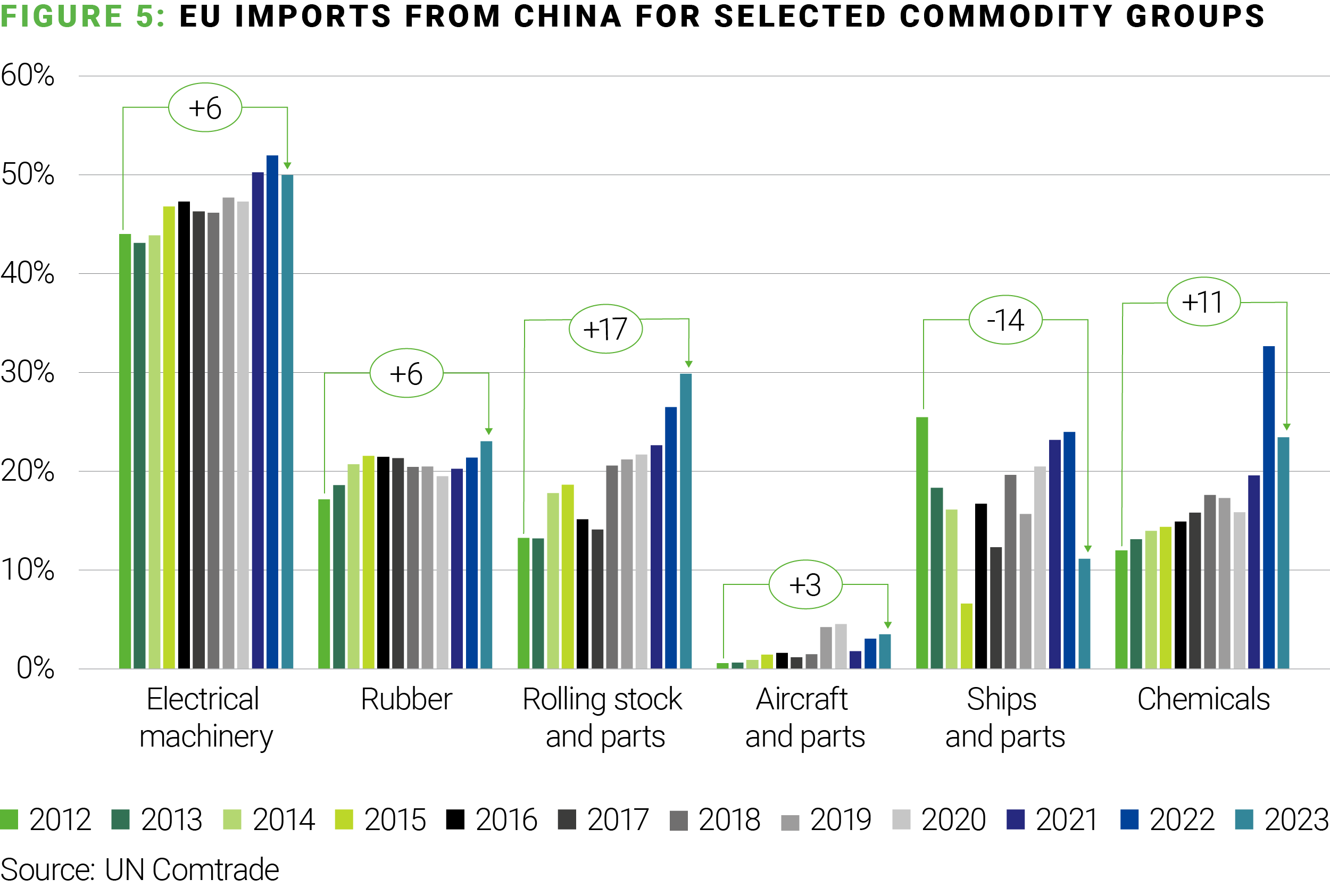

In the global movement towards de-risking supply chains, the focus on minimizing dependence on China has been particularly pronounced in the United States. However, the European Union, with Germany at its core, reached a critical juncture in this endeavor only recently, in 2022. This shift underlines a broader recognition of the strategic necessity to diversify sourcing away from a single-country dependency that has characterized much of the past decades.

As illustrated above, India is seen as the primary alternative for businesses looking to adjust their sourcing strategies in the future, while countries like Vietnam, Mexico, and the Eastern European region continue to gain traction as viable sources for imports. Nonetheless, these alternatives start from a relatively small base, indicating that the journey towards significant diversification is still in its early stages.

Germany’s reliance on Chinese imports spans a vast array of products. This includes not only consumer goods such as smartphones and clothing but also, more critically, intermediate goods and raw materials essential for various sectors of the German economy. The dependency is starkly evident in the importation of certain electronic and electrical components like batteries and accumulators, along with specific raw materials such as rare earth elements. China’s dominant production capacity and available natural resources in these areas poses a considerable challenge for German industries seeking alternatives.

Moreover, many of the critical raw materials imported from China are indispensable for the production of future technologies, including components vital for electric motors, wind turbines, photovoltaic systems, and other green technologies crucial for Germany’s transition towards a more sustainable economic framework.

Despite the clear understanding within the business community of the need to diversify supply chains and mitigate the dependency on critical imports from China, the path forward is fraught with complexity. The process of finding alternative sources is intricate and anticipated to be prolonged, especially for goods where China holds a leading global production role or where alternatives are scarce. This situation underscores the necessity for a strategic and methodical approach to reduce dependency on Chinese imports, balancing immediate economic needs with long-term sustainability and resilience objectives.

As reflected in the earlier table above, the importance of government incentives cannot be understated, with two sectors in particular drawing significant attention in this respect:

Government incentives: Semiconductor sector

The German Government is actively deploying financial incentives to entice semiconductor companies to establish production facilities within the country. This strategic move, particularly in the semiconductor industry, is bolstered by Germany’s desire to become a pivotal node in the global semiconductor supply chain. Given the sector’s minimal labor intensity, the disadvantage of higher labor costs in Germany is offset by the availability of highly skilled labor and the attractive incentives on offer.

Notable investments in this sector include:

All the aforementioned subsidies are pending approval from the European Union. The projects are likely to be supported by the Klimatransformationsfonds (“Climate Transformation Fund”), the “EU Chips Act”, and/or IPCEI (Important Projects of Common European Interest).

Government incentives: Steel sector

The steel industry in Germany is another beneficiary of government subsidies, particularly aimed at addressing the challenges of emissions reduction. The transition to emission-free steel production is supported through significant financial incentives:

These concerted efforts in both the semiconductor and steel sectors highlight Germany’s strategic positioning and commitment to not only diversify its supply chains but also to embrace and lead in the transition towards a more sustainable and technologically advanced industrial landscape.

Government incentives – Battery technology

Europe’s ambition to bolster its technological sovereignty is vividly illustrated by its recent initiatives to localize battery technology and manufacturing. With an eye on electrification and sustainable energy solutions, significant investments, strategic acquisitions, and targeted policy incentives are paving the way for a resilient battery manufacturing ecosystem across the continent.

The landscape for lithium-ion battery (LIB) manufacturing in Europe is evolving, driven by the need for local value creation and European sovereignty over LIBs. Initiatives like the European Battery Alliance, and research programs “Horizon 2020” and “Battery 2030+”, exemplify the concerted efforts to anchor manufacturing within Europe:

These are supported by significant investments aimed at fostering LIB ventures and constructing mega-factories, despite the challenges and competition from dominant Asian manufacturers. In addition, the competitive landscape faces threats from attractive investment conditions in the US. This situation points to the need for EU-wide support and streamlined approvals to bolster continental battery production. Through strategic acquisitions and policy incentives, Europe is actively shaping its energy transition narrative, emphasizing local manufacturing, sustainability, and innovation.

Recommendations

The path forward: Building resilient, cost-efficient, and diversified supply chains.

This approach offers a comprehensive view for executives, emphasizing the need for strategic planning, agility, and leveraging incentives to navigate the shift away from China-dependent supply chains, towards a more diversified and resilient model.