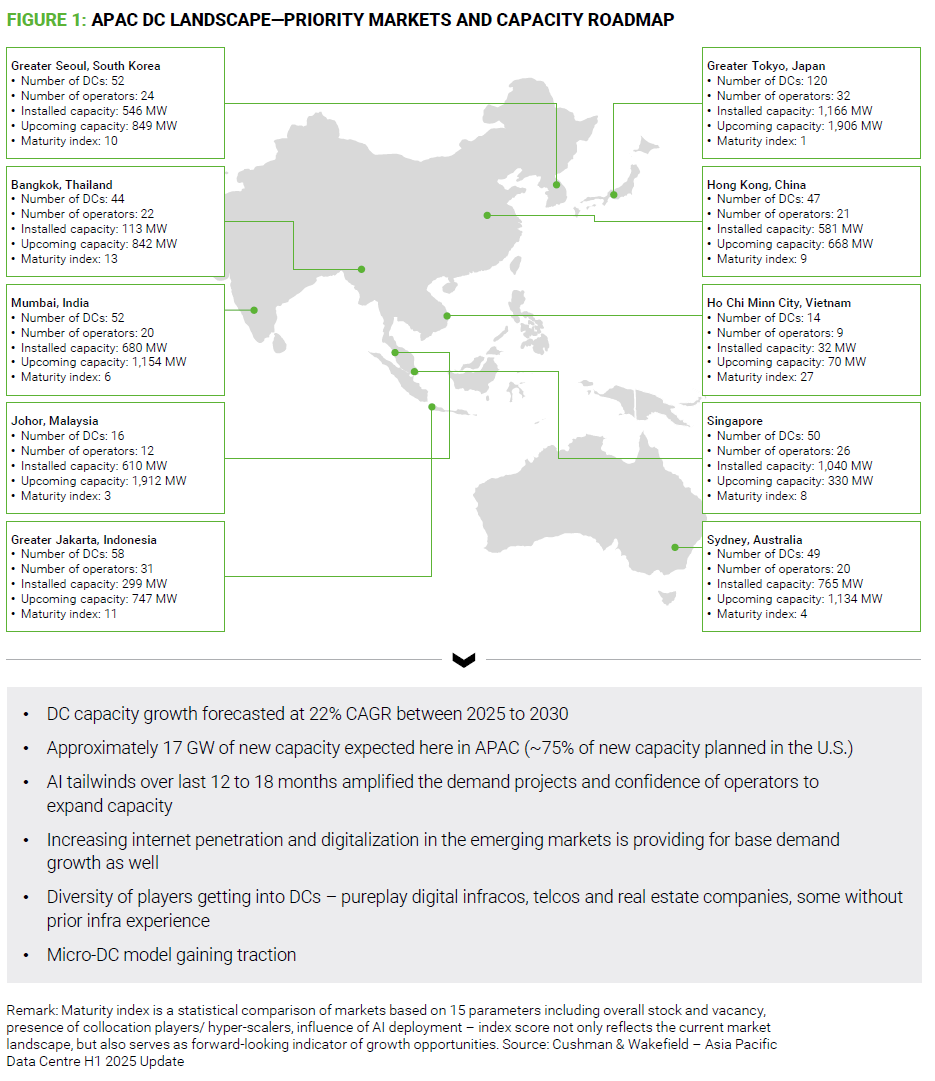

There are several reasons to be excited about the Asia Pacific Data Center (DC) market. Capacity has been growing at 15% CAGR since 2020 and is forecast to grow at 22% CAGR between 2025 and 2030. APAC hosts 62.18% of the world’s population, including markets like India, where GDP growth is forecast to be 6.6% in 2025, citing a strong economic performance. Internet penetration is now at 70.4% and the APAC population is increasingly exposed to digital platforms such as e-commerce, fintech, and social media. In addition, governments are seeking to gain parity on innovation by encouraging digital infrastructure builds. No wonder, then, that several players are entering the DC market in the region—including real estate players, telcos, and pure-play digital infrastructure players. Across the top 10 markets, both capacity additions and new players are coming on board (Figure 1).

However, even with these tailwinds, several challenges make the path to monetization uncertain for APAC DC players.

Key monetization challenges faced by DC operators in APAC:

Demand supply imbalances: Asian markets are facing long Build to Cash cycles. In top markets like Japan, this issue is related to a shortage of General Contractors (GCs), while in other markets, such as India or Malaysia, the time it takes to secure permits before starting construction can slow progress. This results in DC players frontloading capacity when they factor in the interim growth. Further, due to such uncertainty, capacity doesn’t come into the market in a predictable manner—a sudden arrival and glut in capacity will put margins under pressure.

AI uncertainty: As much as AI has been a tailwind for DC operators, forecasting its demand for APAC has been challenging. This unpredictable demand means that operators must now plan for a rack density of 135 kW (and possibly at 600 kW in the future with NVIDIA's Vera Rubin Ultra platform) versus typical cloud services at 15-30 kW and enterprises at 10-15kW. The substantial spike in rack density needed for AI has second-order design implications on floor loading capacity, cooling systems (liquid vs. air cooling), and back-up systems. On the other hand, rapid technology evolution—such as software efficiently enabling emulation of GPU on CPUs—is also driving uncertainty.

Geo-political implications: The rising political tensions between China and the U.S. / aligned West is manifesting in markets like Malaysia where we see parallel infrastructure being set up to service respective customer groups. This leads to higher upfront capex and sub-optimal utilization. Further, access to cutting-edge GPUs is currently limited to hyperscalers, and even if other DC operators are able to secure them to offer GPUaaS (GPU as a Service), the compliance requirements could be onerous.

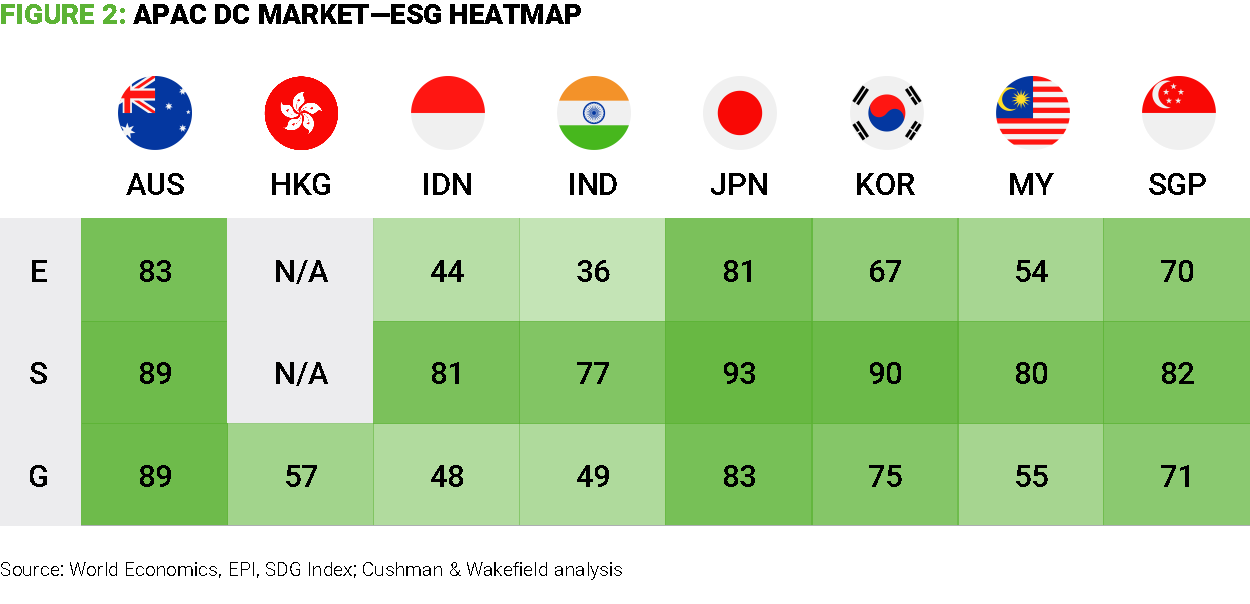

ESG concerns: A number of markets in APAC face water stress and power shortages—the current ESG heatmap in major markets is shown below (Figure 2). Particularly during the summer months, the issues are acute. Furthermore, DC builds are becoming denser, with a capacity of 1000 sqm per MW decreasing to just 285 sqm per MW (estimated from the recent Singapore government allocation of 20 hectares for a DC park). Providing ESG infrastructure (renewable power sources, water treatment plants etc.,) in such high-density developments becomes extremely challenging.

Rising Capex and Opex: Consequently, DC construction costs are high, and factoring in AI workloads will substantially increase these costs. The Capex increase (approximately 20% higher) for high-density racks is not reflected proportionately in rentals (only a premium of 15%). Therefore, operators will need to revisit or harden their business cases for achieving the balance between Capex, Opex, and revenue.

Tenable path to monetization and shareholder returns

Clarifying the path to monetization and improving ROI comes down largely to having a clear strategy up front. We have outlined a few opportunities that need to be explored during the early stages of strategy setting and design for DCs. However, even if the DC is operational, we believe there is a need to revisit and re-vector along the growth, operations, and financial engineering for improved business outcomes.

Differentiate for sustained growth: As soon as the initial or pent-up DC demand is met in a market, the next wave of value capture comes from strategic differentiation. Currently, the hyperscalers take up the base demand at a number of locations. However, these hyperscalers are also highly demanding customers for DCs in terms of custom builds (reducing the reuse value after), rental discounts, contract flexibility, and ESG compliance. In addition, hyperscalers are constantly evaluating build versus lease options in the markets. Therefore, DC operators will need to build a credible source of revenues from local enterprises, local government and public sector segments. This requires a different kind of product development, marketing and sales model. DC operators cannot simply build the racks; rather, they must think about a broader role as digital infrastructure partners as these segments work through their choices of on-prem versus hybrid versus cloud versus sovereign cloud. Further, taking a greater role and accountability in delivering industry-specific use cases (in BFSI, Manufacturing, for example) will help build a more assured and growing stream of services revenues. DC operators are not currently set up for capabilities to target these segments—therefore, they should seek to partner with telcos and System Integrators (SIs) for faster time to market.

Drive operational excellence: DC operators in APAC are aware of or have mostly squeezed out the value from traditional cost levers of, for example, Power Usage Effectiveness (PUE) optimization or better chillers. The next frontier of value creation we see is around form factor and operating model choices. For instance, a number of DC players are focusing on Tier 1 locations within a market—for instance, Mumbai (India) or Johor (Malaysia). While there are benefits of an ecosystem and connectivity, it becomes costly to build and, operationally, expensive to run. An alternate operating model here can be to focus on Tier 2 locations within a market, especially if target customer workloads are latency tolerant. In some markets, an economically viable set of industries and customers may still be present in Tier 2 locations. Secondly, accessing better layout and securing permits may be easier, as distributed DCs put less strain on the power grid. Further, building modular DC blocks versus a large complex one has its advantages. The reliability (which increases both Capex and Opex for higher grades) can be custom provided with better segmentation of workloads. For instance, AI training / backup workloads can run on best-effort reliability blocks while critical core applications run on Tier 3+ reliability blocks. Modularity also comes in another form, where heat is extracted more efficiently from containerized server blocks rather than cooling entire giant rooms. There are also operational improvements that can be made in partnership with the customer, such as GPU-aware cooling and load scheduling.

Engineer financial outcomes: Capital efficiency and risk mitigation are key pillars that DC operators focus on. Modular builds help drive up the productive use of infrastructure and capital. An ROI-focused pricing mechanism that helps promote early / at-scale commitments (such as anchor tenancy, zero capex migration etc.) with menu options for the granular functionality and features helps improve the yield. Operators are also advised to take yield management approaches similar to airlines or hotels, where there is a pricing model that adapts with the ecosystem density. Further, there is also a phased window where some services are provided as “loss leaders” and pricing leverage is exercised as customer stickiness improves. During the strategy phase, it is key to have a clear exit strategy, with the triggers well laid out—particularly for smaller players. Finally, for those DC operators who seek a multi-location portfolio, it is key to test the option of sale and lease-back. This helps free up capital, even as operational scale is achieved.

Conclusion

DC operators in APAC are facing a new reality—demand is rising, but monetization is becoming harder. The region’s digital momentum is undeniable, but so are the challenges that come with it, from AI-driven complexity to rising sustainability pressures. Success in this evolving market will hinge on how well DC operators, big and small, can adapt—by rethinking their growth models, embracing modular and efficient designs, and engineering their finances smarter. Those that look beyond the race for capacity and focus instead on creating differentiated and reality-aligned operating models will be the ones to survive and truly unlock the promise of APAC’s digital decade.

About the authors

Sai Tunuguntla is leader of the Telco, Media, and Technology practice for AlixPartners here in APAC. Sai has more than 20 years of consulting experience, serving clients across both emerging and developed markets here in APAC and the rest of the world. Sai brings “zero-based” approaches to operational excellence and has worked with clients building practical growth strategies.

Pritesh Swamy leads the Data Center Research and Advisory Services across APAC at Cushman & Wakefield and is based in Singapore. With more than 21 years of experience, Pritesh supports data center clients in understanding market dynamics, identifying trends, and advising a diverse set of stakeholders to make informed decisions regarding investments and operational decisions.

AlixPartners and Cushman & Wakefield have collaborated and recently launched the DC360 proposition to serve data center clients on their growth, operational excellence, and finance agendas.

For further perspectives on U.S. and EMEA DC markets and how some of the issues discussed in this article may have commonality in those markets, refer to AlixPartners' 2026 Data Center Market Outlook.