People

Jason McDannold

Americas Co-Lead, Private Equity, Partner & Managing Director

Chicago

People

Jason McDannold

Partner & Managing Director - Chicago

We expect private equity and growth investors to focus on three areas of opportunity in 2026:

After a cautious two years, private equity investors are returning to growth, but with more precision. Dealmakers are concentrating on sector-specific theses that combine recurring revenue, operational value creation, and defensible market structures.

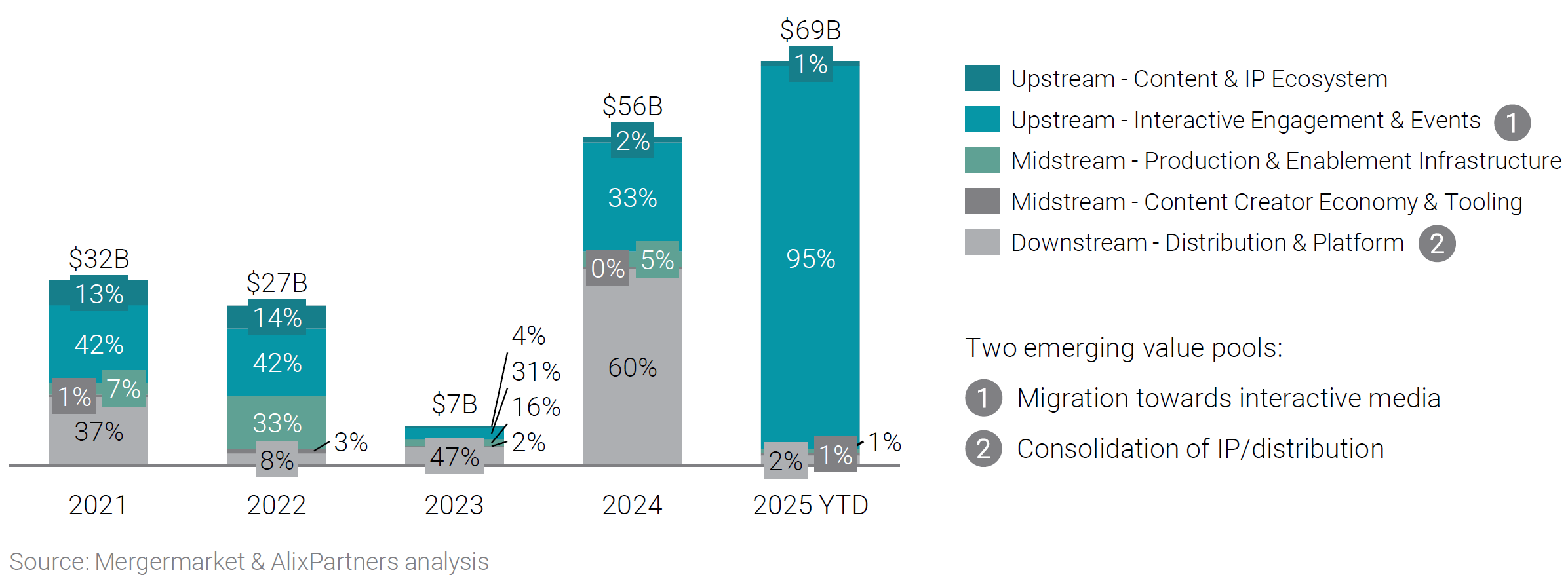

This shift is especially observable in the media industry, where private capital is increasingly focusing its attention. Deal value rebounded sharply in 2024, but this surge centered on a handful of large-scale, high-conviction transactions such as Silver Lake’s investment in Endeavor, EQT’s $2.8 billion acquisition of Keywords Studios, and KKR’s $1.7 billion investment in FGS.

The rise in average deal value underscores a strategic evolution: Private capital is consolidating around fewer, more durable themes such as scalable ecosystems and infrastructure that balance durable value with growth. Within media, two themes have emerged as the anchors for this next cycle—interactive media and consolidation of IP/distribution.

Private equity is concentrating on two key media value pools: interactive media and consolidated IP/distribution. Interactive ecosystems—encompassing gaming, live events, esports, and fan engagement—benefit from AI, real-time rendering, and automation, as well as data-driven, commerce-linked monetization. Deal values in these areas have surged 3–4x since 2021. Meanwhile, consolidation of IP and distribution by studios and aggregators, such as Disney-FOX and Warner Bros.-Discovery, raises entry costs but secures audience control. PE is increasingly focused on scalable infrastructure and tooling around these sectors, favoring strategic partnerships and co-financing over full-control acquisitions.

Global private equity announced media total deal values ($B) by subsector

Private equity will focus on the infrastructure powering content interaction and monetization. Upstream investments include gaming services and live engagement platforms, exemplified by EQT’s $2.8B acquisition of Keywords Studios. Midstream opportunities include scalable creative tooling, AI-enabled ad tech, and agent-ready content infrastructure, as shown by Novacap’s $1.9B IAS acquisition. Co-financing or partnerships with premium IP and distribution platforms provide indirect exposure to high-value content, demonstrated by Domain Capital Group’s slates with Warner Bros. and Paramount. By targeting these recurring-revenue assets, PE can capture value from engagement-driven media, independent of which major studio controls content.

As content ownership concentrates, the most durable opportunities lie in the connective infrastructure—tools, services, and monetization engines that enable audience engagement and content delivery. By investing in scalable, recurring-revenue middleware and interactive ecosystems, private equity can build defensible businesses that profit regardless of which studio owns blockbusters, securing a central, enduring role in the evolving media value chain.

The media and entertainment world is shifting faster than ever—from streaming platforms merging short-form, long-form, and live content, to AI upending search and gaming, and M&A activity reshaping the landscape. Our annual Predictions Report dives into these trends, exploring who’s leading the charge, what’s next, and how businesses can stay ahead in a market defined by change. Click through to see where the industry is headed—and where opportunity lies.