Andrew Bergbaum

Global Co-Leader of Automotive & Industrial, Partner & Managing Director

London

Andrew Bergbaum

Partner & Managing Director - London

Successfully shifting from fossil fuels to full electrification is a challenging enough objective for the automotive industry to wrestle with during the decade ahead. The fact that the 2020s began with a pandemic has only served to accelerate the need for industry transformation, as the monumental impact of COVID-19 brought many more disruptive macroeconomic issues to the fore.

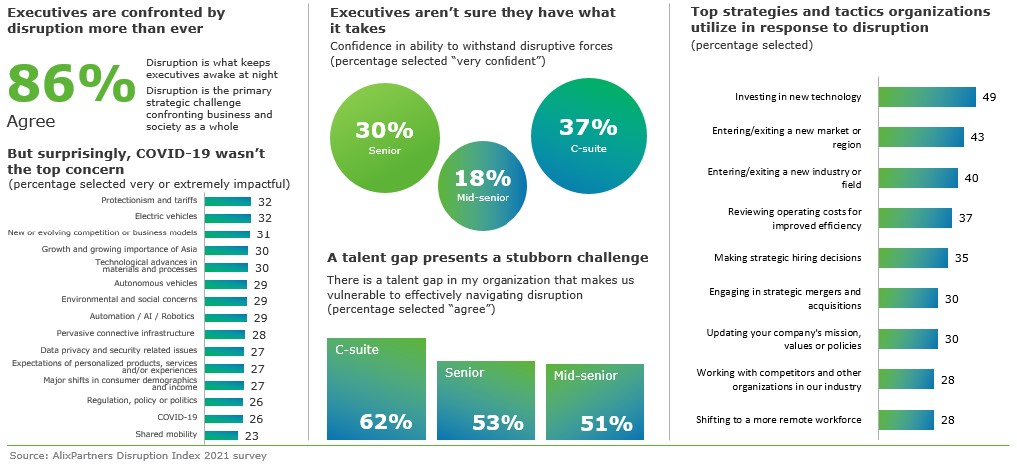

This year’s AlixPartners Disruption Index reports that COVID-19 features low down the list of top concerns for automotive executives, but there is little doubt that the events of 2020 have magnified the intensity of the other trials ahead. Indeed, respondents in the industry display confidence levels some way below the all-industry global average when it comes to their businesses’ ability to withstand disruptive forces, with less than a third reporting high confidence in this area.

We were told that protectionism and tariffs, electric vehicles, and new or evolving competition or business models are the top three issues keeping executives awake at night. It is a trio of intrinsically intertwined challenges, all present before COVID-19 struck, but since supercharged from the events of the past 16 months.

Supplier shortages and shifting consumer preferences

Showroom shutdowns and a drop in demand presented automakers with the headache of accurately anticipating the timing and level of industry uptick. Further, manufacturing plants were brought to a standstill at times, as a worldwide semiconductor shortage set in, stifling OEMs’ ability to return to full production during the second half of last year. As forecast in our 2021 Global Automotive Outlook, the cost of this stuttering restart, specific to semiconductor availability, is expected to cost automakers around the world nearly four million light vehicles of lost production, worth $110bn.

These direct economic impacts are stark, at a time where the evolution to a cleaner automotive future – and the huge levels of enabling investment required – is dominating the long-term roadmaps for every player in the industry, governments, and consumers.

Changes to consumer behaviour because of the pandemic, including increased financial concern and heightened environmental awareness, will continue to adapt the automotive landscape in terms of length of vehicle ownership and number of vehicles owned per household. This appears to be of particular concern in China, where 50% of respondents identified changing consumer demographics as being very or extremely impactful, versus 27% globally. The online second hand car sales market is also booming, and as cost and infrastructure barriers around electric vehicle adoption persist and the uptake of alternative emerging micro-mobility models increases, it’s clear that there is yet more disruption in the market for OEMs to contend with beyond COVID.

The need to deliver on technology - and talent

Disruption Index respondents cited investment in new technology as the top strategy to counter disruption. With all roads leading to electric in the future, this may come as no surprise, but adjacent to this is a firm focus on better strategic hiring decisions. Our study told us that 62% of automotive C-suite respondents agree that there is a talent gap in their organisation that makes them vulnerable to effectively navigating disruption.

As traditional manufacturing and technology continue to converge in automotive, digital and tech skillsets are becoming increasingly desirable to catalyse and effectively manage transformation efforts. However, all industries are now driven by a digital-first mentality and the battle for the top talent will only intensify over time.

Perhaps this eye on where talent will need to over-index in the future is why 48% of respondents expressed concern over job security – most acutely observed in Japan at 77%. Long periods of enforced human absence (or much reduced) from manufacturing plants due to COVID restrictions have seen an acceleration in integrating artificial intelligence equipment that increases efficiency and effectiveness during production, also carrying employment implications.

Suppliers will come under increasing pressure to adapt under, in some cases, the existential threat of an electric future, where powertrain component complexity drops dramatically and electrical operability and connectivity needs continue to rise. COVID-19 has highlighted that any fragilities in supply chains can have catastrophic consequences, and OEMs will do as much as they can to develop strategic alliances to shore this up for the future, strengthening purchasing power and aligning with the optimal network of innovative partners who can help them deliver on the bold electric visions they have set out.

Ambitious targets require boldness in transformation

Global industry sales data suggests a strong post-pandemic recovery to date, spurred on by a positive macroeconomic outlook, but a return to pre-pandemic volumes is likely to be at least four years out. The need to maintain strong revenues now to fuel investment in electric means the race is already on to emerge as a new-world winner when government EV targets for 2030 are on the immediate horizon and OEMs’ individual targets for electric propulsion share are being counted.

As consumer preferences continue to shift, the prize is immense for developing the right product at the right price that can also deliver healthy profitability after such heavy up-front investment.

In times of such intense disruption, the need for transformation is inevitable. The automotive market leaders that emerge in the all-electric world will undoubtedly have displayed the agility, innovation and speed to action to harness the huge opportunity that now exists.