Michael Crisanti

Partner & Managing Director - Chicago

Markets are stress-testing valuations of software companies with the wrong question. A wave of "vibe-coding" demonstrations, using AI to spin up a working replica of a product in an afternoon, has boards and investors asking the same thing about every software business: Can AI just rebuild this?

It’s an understandable question, but it misses the mark. Recreating an interface only tests whether software is replicable, and essentially all software is. The question that decides who survives is more difficult: When agents rather than humans are the end users, does the value stream still hold?

The term we use to ground this question is the value pivot. It has become the lens we employ to understand the future potential of a software company, whether the goal is to put a number on what it's worth or to decide how to run it. Those usually get treated as separate problems, one for investors and one for operators. In reality, they are the same problem seen from two chairs: Both come down to where a company's value will be once the work is done by agents.

Start from the key premise that recreating software as it exists today is a losing proposition, because the value delivered by the software is going to change. The interfaces, the workflows, the per-seat pricing: Most of it sits in the wrong place in a future world where agents do the work. Hence, betting on today's product is betting on a snapshot. It's the instinct Wayne Gretzky made famous with his quote “Skate to where the puck will be, not to where it is now.” Testing whether you can recreate today's software chases the puck; the value pivot focuses on where the puck will be once agents are the users.

To get there, you must decompose the value rather than defend the current product. This means breaking down and understanding what a business is worth to its customers and continually re-pointing the company at that worth as the market moves. At one point, both Netflix and Blockbuster mailed DVDs to customers. But then one decomposed the value it truly provided (delivering content to the viewer) and kept pivoting toward it (from streaming to producing and owning the content outright). The other defended its existing retail model and became a memory.

Netflix's core was never the disc or the website; it was the content and the rights behind it, and the company kept finding better ways to deliver it. That discipline is critical but is too often the exception, not the rule. Most software companies innovate once and fall in love with the product, spending years protecting what the software does today instead of the problem it solves. It's the founder's trap, and the forthcoming agent era is about to make it fatal.

Rather than make a single prediction and defend it, we built a way to identify where a company's value sits today, where it's likely heading over the next few months, and what companies must do with that information. We then run this model repeatedly as the ground shifts. The output isn't an answer with a shelf life; it's a discipline that keeps producing new answers.

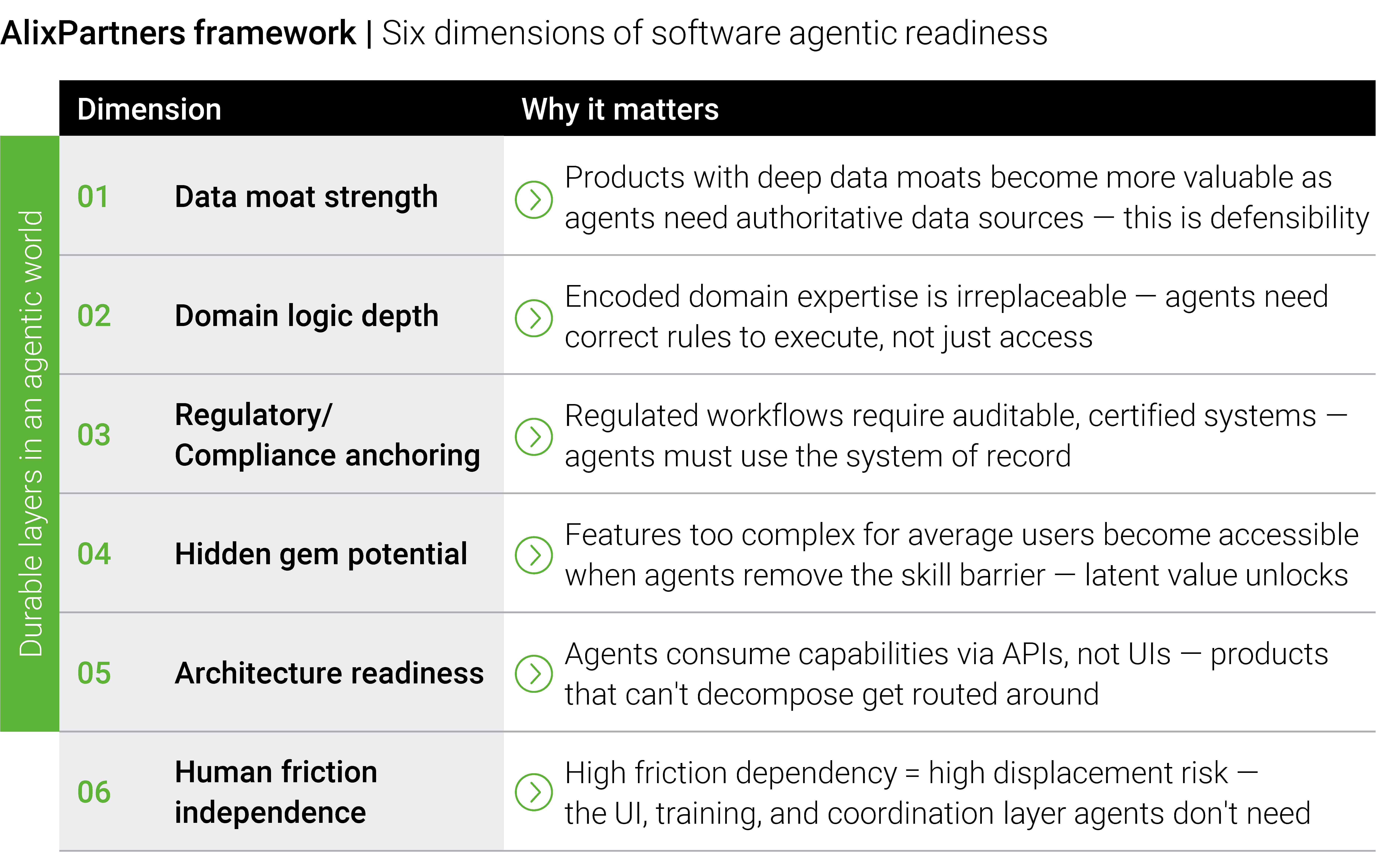

Run this discipline across enough companies and patterns emerge. In doing so, we’ve found that there is enormous, durable value inside nearly all software businesses. The domain logic and the proprietary data, representing everything a product uniquely knows about its industry, aren't going away. They'll simply be delivered in different ways to different consumers.

The catch: most of that value is currently trapped. Across a portfolio, roughly 70 percent of a product's worth sits in durable layers. Yet the weakest dimension we measure is a product’s architecture. The value is trapped behind interfaces built for human hands, behind legacy technology and architectures that were never meant to be exposed. Own the data, the domain logic, or the transaction itself, and you can stay valuable in an agentic world, even if who delivers that value changes.

Unlocking this trapped value is the real work that the value pivot calls for, and it can be uncomfortable. If the value is durable but moving, then the company and the investor weighing it both must stop blindly defending the current product and look hard at where that value will be delivered in the future.

Answering honestly may mean letting go of what you fell in love with about the product. That's the hardest part, but the most important.

Once we’ve answered these questions, the focus turns to portfolio management. Most leaders already sort their products into “grow,” “sustain,” and “sunset;” the value pivot turns that same lens inward and takes it one level deeper, analyzing the individual capabilities inside each product. It assesses which to invest in, which to hold as cash cows, which to retire, and which hidden gems to mine for growth.

Two critical decisions emerge immediately:

Pricing is the final place the pivot shows up, and it is the most revealing. Of the more than 50 companies we've assessed, only one prices on the value it delivers today by billing per outcome rather than per seat (and even that one is being commoditized). Most still sell seats and subscriptions, models that rely on a human as the user. Nearly all will have to change. Harder still, almost none can yet measure the value they will need to bill for. Saying you price on value is easy; instrumenting it today is nearly impossible. This is why it will initially be a moat for whoever gets it right first.

None of this requires predicting the next turn of the market. It requires knowing that your value will move and building the muscle to move with it before your competitors do. That's the value pivot. Whether you're deciding what a software company is worth or deciding how to run one, it comes down to that same question: Can the value it contains be effectively and continuously delivered in an evolving future?