People

Jeff Goldstein

Partner & Managing Director, Americas Leader, Technology, Media, and Telecommunications

Boston

In 2026, we predict more than $80 billion in media M&A deal value, with sustained increased volume across all quarters. This will be driven by a broader resurgence in M&A activity across large and small deals as media companies adjust to a new economic normal and consolidate legacy assets while investing in new technologies.

Last year in this report, we predicted that media M&A activity would rebound in 2025, driven by reduced regulatory scrutiny and lower capital costs that would improve conditions for dealmaking and fuel additional spinoffs of cable assets.

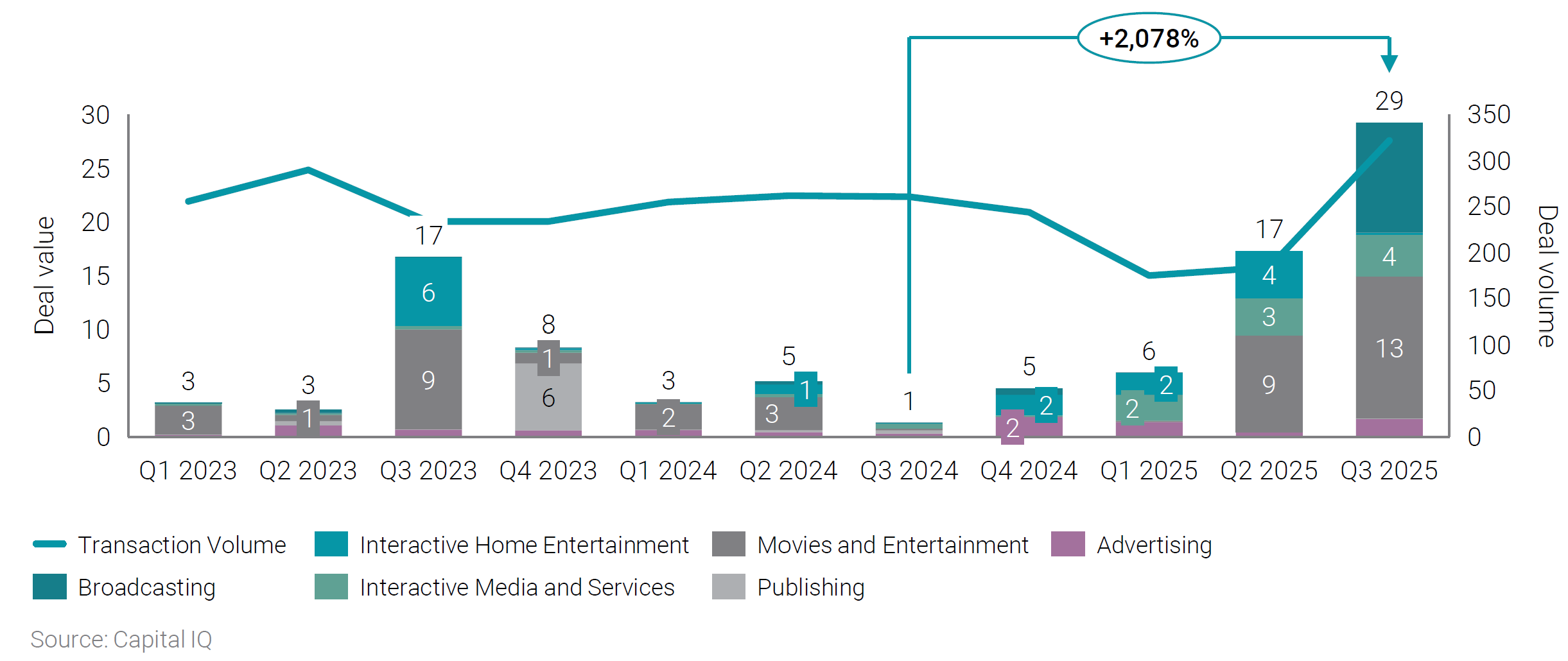

Despite a slow start to 2025, this prediction has proven accurate. In Q3 2025, we saw closed transaction value increase by more than 2,000% compared to Q3 2024, led by media holding company mega mergers and cable TV carve-outs.

Falling interest rates and private equity’s deep involvement set the stage for heightened media M&A in 2026. Goldman Sachs predicts multiple rate cuts will lower the terminal rate to 3–3.25%, creating favorable financing conditions. Media firms that act decisively on acquisition targets will benefit, while hesitation risks losing opportunities to competitors or financial buyers. Surveying the market, conducting thorough due diligence, and executing transactions efficiently will be critical for success as companies aim to navigate a post-rate-hike, capital-rich environment.

Media transaction value and volume by quarter (Q1 2023 – Q3 2025, $B)

Regulatory shifts are reshaping deal dynamics, particularly in linear TV. The July federal appeals court ruling lifting the FCC’s ownership limits for top-four stations encourages aggressive consolidation. Deals like Nexstar’s $6.2 billion Tegna acquisition and Sinclair’s broadcast merger highlight this opportunistic stance. With over $500 billion in uninvested global PE capital, both strategic and financial buyers are actively pursuing assets, especially those that strengthen linear TV portfolios. Media companies will need to evaluate carveouts and asset sales quickly to capitalize on this favorable regulatory and capital environment.

AI and evolving media consumption are driving increased M&A activity, with smaller, tech-focused deals prioritized. Companies seek assets that enhance advertising, content automation, and workflow efficiency to remain competitive. Recent industry commitments—WPP’s £300 million, Publicis €900 million, and Reuters $200 million annually for AI—illustrate this trend. Acquiring AI capabilities through M&A is now critical, as lagging companies risk falling behind. In 2026, media firms must determine their role as buyers or sellers, identify targets, and strategically position themselves to benefit from this second wave of technology-driven, high-value media transactions.

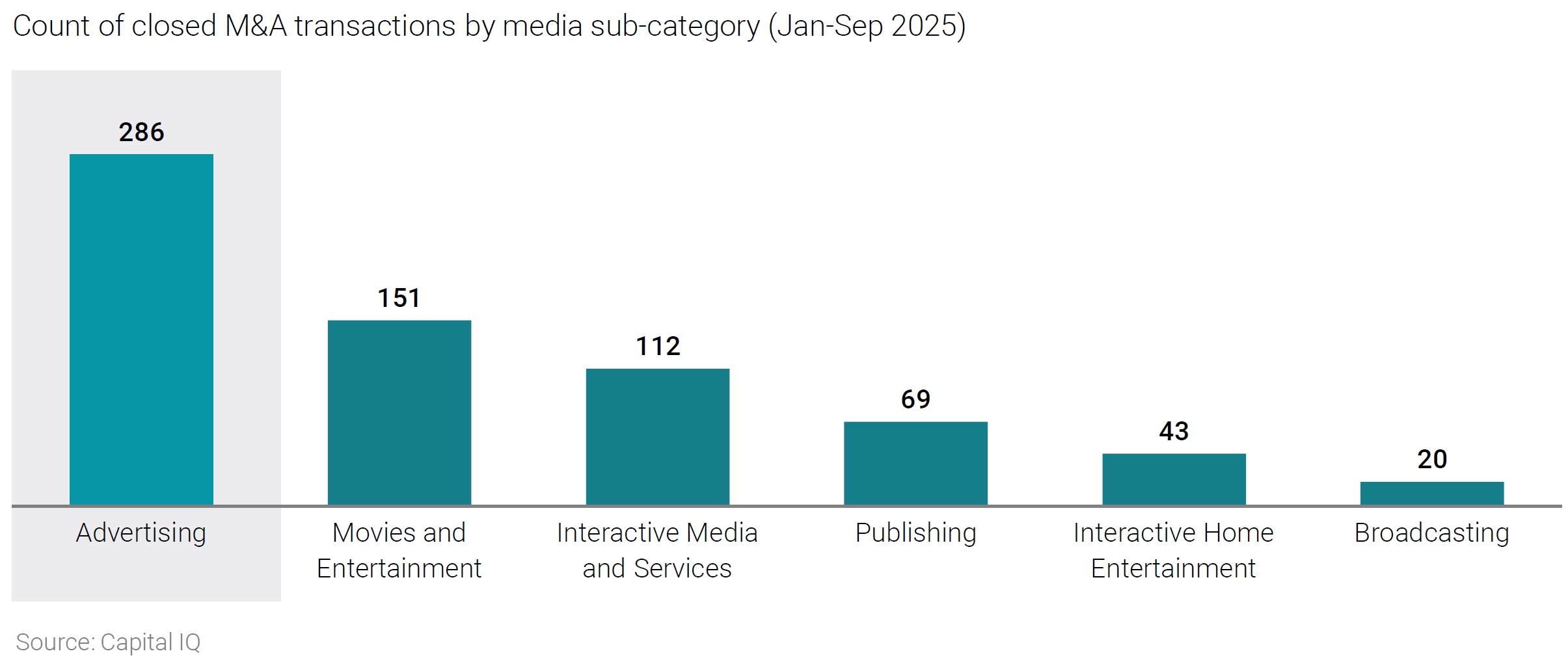

In 2025, advertising deal volume far outpaced other categories

The media and entertainment world is shifting faster than ever—from streaming platforms merging short-form, long-form, and live content, to AI upending search and gaming, and M&A activity reshaping the landscape. Our annual Predictions Report dives into these trends, exploring who’s leading the charge, what’s next, and how businesses can stay ahead in a market defined by change. Click through to see where the industry is headed—and where opportunity lies.