Offshore supply vessel companies face continued pressure, according to AlixPartners study

NEW YORK (September 24, 2018) – Offshore supply vessel (OSV) companies continue to face pressure due to a radically changed oil industry and must take quick and decisive action in order to survive in what should be considered the “new normal,” according to a new study from AlixPartners, the global consulting firm.

Despite the recovery in oil prices, the OSV industry remains in trouble. Charter rates across most asset classes and regions are still running at or close to operating cost levels. There is a continued glut of vessels, caused by over-ordering during the boom in oil prices and easily accessible bank credit, hampering the industry. Companies hoping for a dramatic rebound in OSV vessel demand are playing a dangerous waiting game, as their existing financial resources are likely not enough to sustain them through the current environment. According to the AlixPartners analysis, 34 of 38 companies had Altman-Z scores of less than 1.8, indicating a high likelihood of bankruptcy in the next 12 months.

“It is abundantly clear that OSV operators need to face the music on the current state of the market and the real probability that we won’t be heading back to sustainable industry dynamics without a structural change to the sector,” said Jeff Drake, Managing Director at AlixPartners. “Companies need to be disciplined about capacity management and do everything they can to reduce costs and increase operational efficiency.”

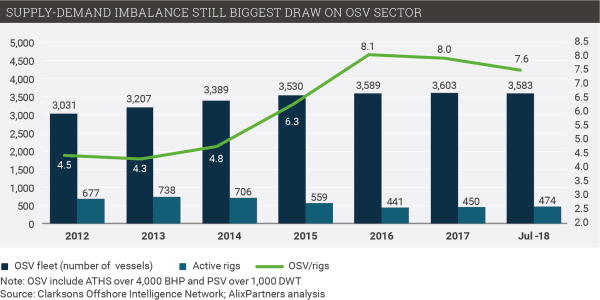

The two factors that drive revenue for OSV companies remain offshore rig utilization and day rates. The number of active offshore rigs is 33% lower than 2014 levels, declining to 474 in July 2018 from 706 in 2014. OSV day rates are 40% lower than in 2014. Geopolitical factors and US oil infrastructure issues aside, abundant shale oil supplies in the near term and the impact of energy transition on oil demand in the medium-to-long term will likely serve as constraints on drilling a substantial number of new offshore wells.

Given these structural shifts in the oil industry, the global OSV market seems currently oversupplied by about 1,150 vessels. About 900 vessels are 15 years or older which will have difficulty finding work and could be retired, as newer vessels are more efficient, less costly, and more compliant with increased environmental regulations.

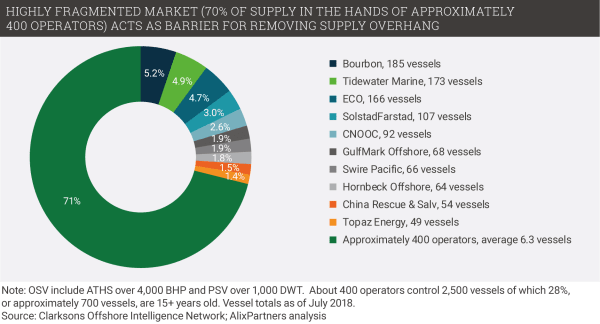

But there are real factors preventing a reduction in the overall supply of vessels. Chiefly, the sector is fragmented, with the largest operators controlling 30% of the fleet and the remaining 70% controlled by 400 smaller operators with fleets of six or fewer vessels. Small operators have little incentive to retire any of their own fleets and are loathe to take action that would benefit the larger companies or the sector overall.

Recommendations

Presently, operators are price takers in the market at rates at or close to operating expenses. Companies will need to be more ambitious about their cost-cutting plans, by streamlining both operating and selling, general and administrative (SG&A) expenses. Some of which to be driven by employing state-of-the-art technology.

Consolidation will likely play an increasing role to address some of the apparent supply overhang while realizing cost synergies and in turn improving the sector’s value proposition. On the other hand, debt restructurings seem still off-limits for some creditors. The fact remains, though, that with a debt/EBITDA ratio of 23.9x, the sector is overleveraged, most of that debt is unlikely to be repaid.

The difficult and painful actions that are required now to become more cost-competitive and restructure balance sheets could create stronger world-class companies that can not only survive this crisis, but even thrive if the sector recovers.

For additional information see our paper, “Too many ships, too few rigs: why recovery is still a distant dream for the OSV sector.”

About AlixPartners

AlixPartners is a results-driven global consulting firm that specializes in helping businesses successfully address their most complex and critical challenges. Our clients include companies, corporate boards, law firms, investment banks, private equity firms, and others. Founded in 1981, AlixPartners is headquartered in New York, and has offices in more than 20 cities around the world. For more information, visit www.alixpartners.com.