People

Randy Burt

Americas Leader, Consumer Products, Partner & Managing Director

Chicago

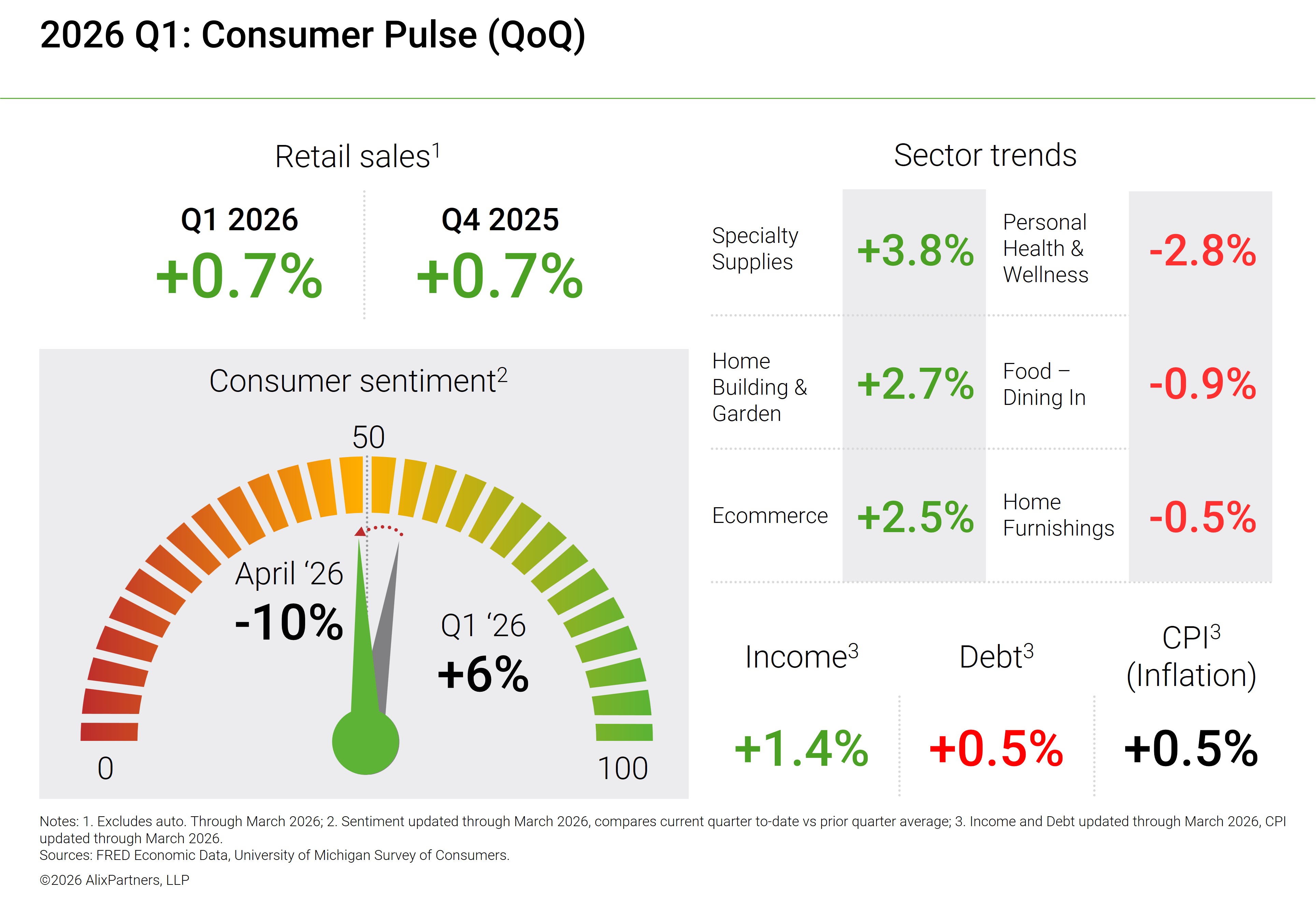

Retail sales were modestly stronger in Q1 2026 versus the previous quarter, with overall retail trade up around 0.7%. Specialty supplies grew a solid 3.8% and home‑building and garden rose 2.7%, while other discretionary categories such as health & wellness and dining out saw minor declines as consumers prioritized project‑ and home‑related (home building & appliances) spending.

Income, CPI, and debt show a consumer still spending but under growing constraints: income rose around 1.4% quarter‑over‑quarter, CPI increased 0.5%, and debt edged up 0.5%. Together, this mix supports steady but cautious spending, though consumer sentiment slipping to a record low in April to date could paint a different picture in the coming months.

On a monthly basis, AlixPartners charts sales, sentiment and supply chains in consumer-facing businesses. Learn more about the Consumer Products Corner newsletter and read previous articles, here.