Marcello Bellitto

Partner & Managing Director - Milan

The rise of generative and agentic AI is bringing down the curtain on a golden era for SaaS providers, heralding challenging times ahead for many businesses and their private equity sponsors or investors.

As this new technology accelerates a split between resilient SaaS platforms and vulnerable mid‑market vendors, we outline the risks for PE sponsors and lenders – and the actions that will matter most in the coming refinancing cycle.

Seat-based pricing strategies have driven predictable, recurring revenue for nearly two decades. However, they no longer make sense from provider or customer standpoints, in a world where some AI systems can perform work equivalent to hundreds of human agents. As we recently reported, the sector is beginning to shift toward consumption- or outcome-based models that better reflect how AI software creates value.

Competition is also increasing, from hyperscale platforms at one end of the scale to AI-native start-ups at the other. There is also growing competition from outside the conventional SaaS space. Cheaper, faster AI-driven software development means the businesses that have traditionally been SaaS customers may now expand their in-house AI capabilities. At the very least, this AI-led disruption will give these customers more bargaining power at contract renewal.

An uncomfortable truth for not only the software sector itself but also the PE firms that sponsor so many providers within it – and other invested financial stakeholders with private credit who play a large role – is that some will be unable to withstand the disruption ahead. While we are yet to see widespread defaults, software valuations have declined significantly from peak levels. Investor concern is evident in the number of software loans being offloaded at a discount, amid fears of defaults down the line.

PE exposure to AI disruption in the European SaaS sector

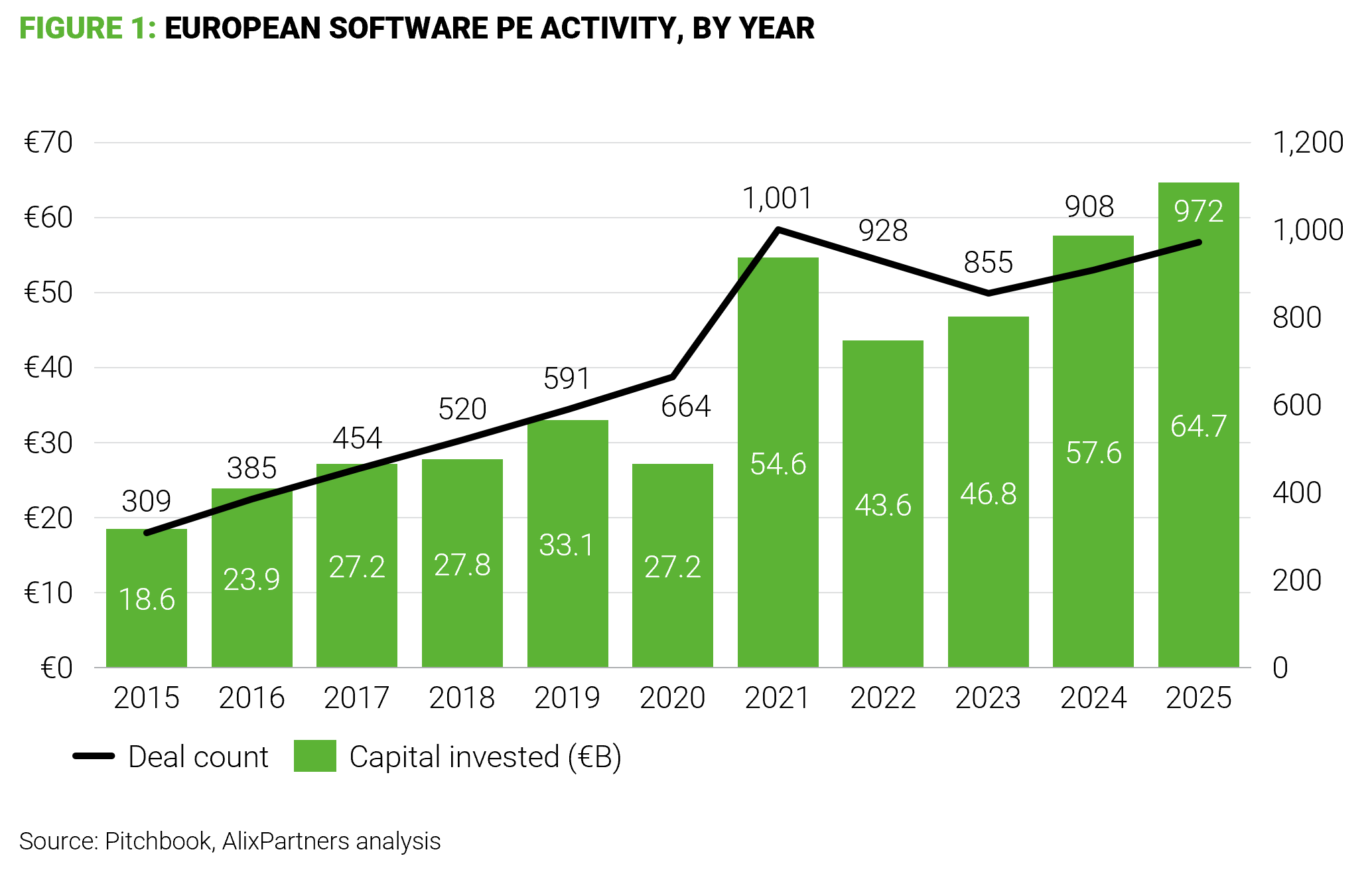

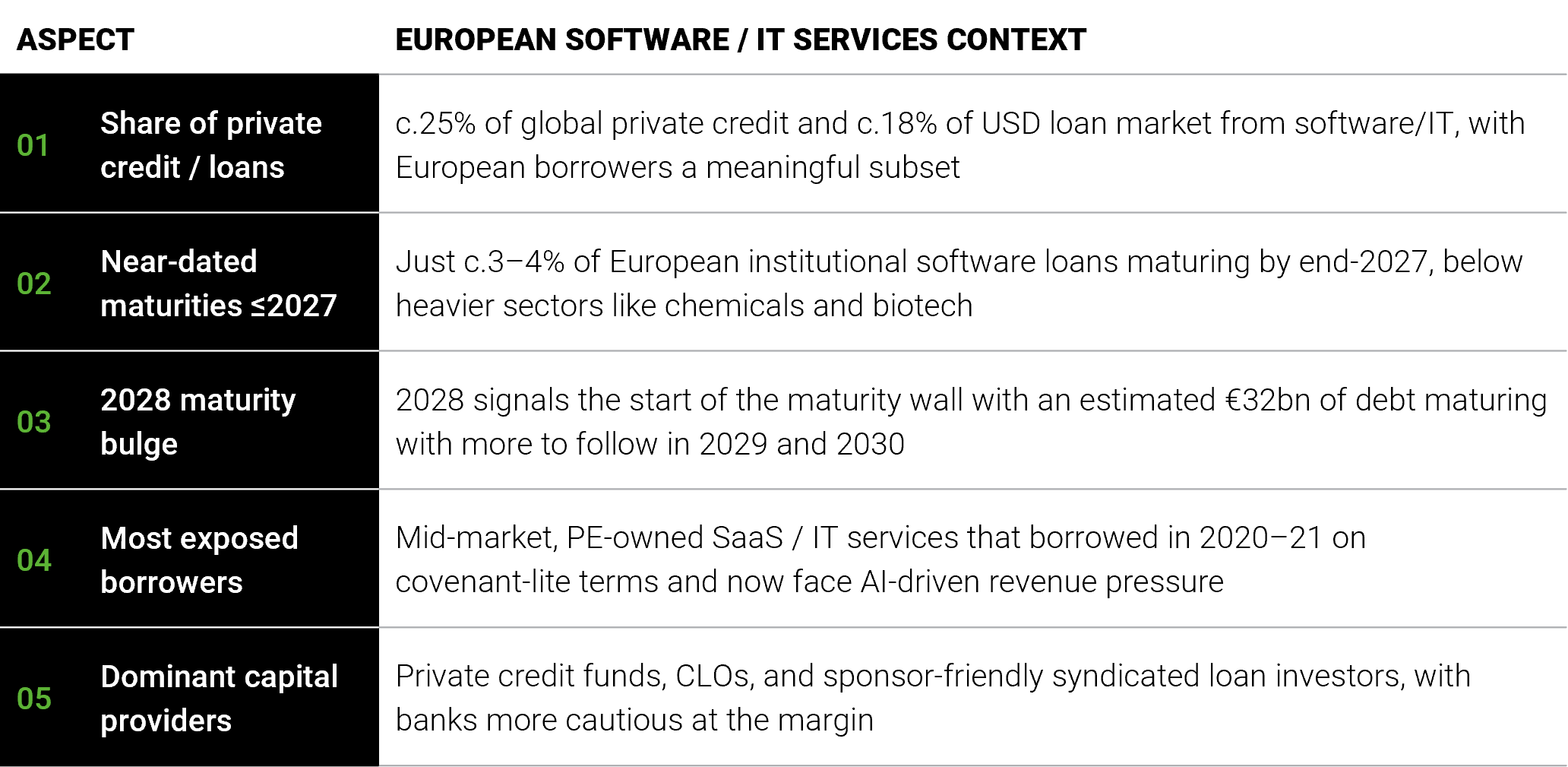

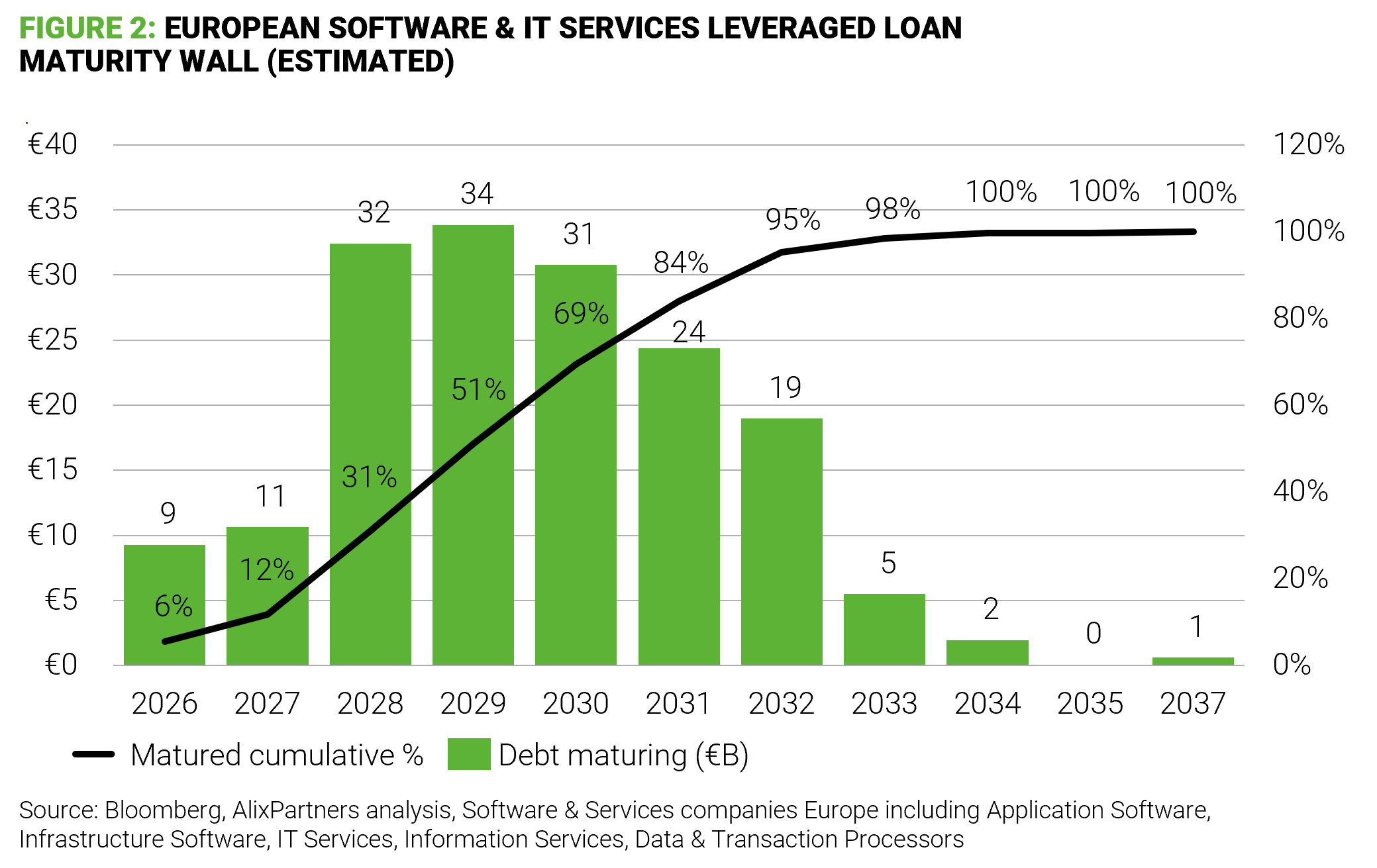

Few sectors rely so heavily on leveraged finance and private credit markets as software. Along with IT and broader tech, software now represents c.25% of the entire private credit market and c.18% of the USD leveraged loan market, according to data from credit platform Octus. In Europe specifically, software accounts for around 7% of the main leveraged loan indices by sector weight today, but its share increases to c.10% of the sizeable 2028 “maturity wall”, with roughly €7-8 billion of software loans alone due by the end of 2028, with a large portion originated in the 2020–21 low‑rate window.

In Europe, the enterprise software sector has been one of the most active areas for private equity investment.

The issue now is twofold. First, there is the unprecedented speed, scale, and impact of AI disruption – as we saw, for example, when the launch of a single Anthropic plug-in sent share prices of European legal software providers tumbling.

Second, the funding stack for these businesses spans covenant‑lite syndicated term loans, sponsor‑backed unitranche and senior/second‑lien private credit and, to a lesser extent, high‑yield bonds, with private credit funds and CLOs now the dominant holders of risk.

Differences between U.S. and European exposures

Exposure is most concentrated among mid‑market, PE‑owned SaaS and IT services platforms that leveraged up in 2020–21, often at high purchase multiples and with minimal amortisation, leaving a cohort of loans that become current in 2027–28 just as AI applies material pressure to many of their revenue models.

This points to a pronounced maturity wall on the horizon and, while exact estimates may vary, it is of considerable scale. Across European leveraged finance, more than a quarter of all loans now cluster in 2028 alone – the largest three‑year forward bulge seen since before the global financial crisis – with software and IT services accounting for a disproportionate share of that single‑year spike, relative to their share of nearer‑dated maturities.

For lenders, that means that a wave of necessity‑driven refinancings, amend‑and‑extend deals, and selective restructurings will need to be agreed 12–18 months in advance, at a time when performance dispersion inside the SaaS and IT services universe widens, and the underlying AI disruption makes underwriting future cash flows materially harder.

On a relative basis, the U.S. credit system is more exposed to SaaS than Europe. Software and IT represent close to 18% of the U.S. leveraged loan market and more than 12% of U.S. broadly syndicated CLO collateral, compared with less than 10% in European CLOs.

The U.S. software maturity stack is also more front‑loaded into 2026–28 and skewed toward lower ratings, with roughly half of loans at B‑ or below, heightening sensitivity to any further AI‑driven slowdown.

Sector bifurcation – and what it means for mid-market operators

While there is little evidence so far of widespread financial underperformance across the software sector (market activity is more likely to be driven by multiple compression), mid-market operators perhaps have most to fear.

According to our 2026 Enterprise Software Technology Predictions Report, in 2023, 56% of mid-market companies were expected to grow by at least 15%; now that figure is only 22%.

Meanwhile, venture capital continues to flow into AI start-ups at unprecedented levels. Our 2026 study also found that global investment in AI-focused companies accounted for 53% of all VC funding worldwide in 2025, with roughly $150bn of investment in AI companies in the first three quarters of the year.

The size of tech giants’ bets dictates the mid-term direction of travel. Investments are driving new technologies in-house, raising the bar for speed and scale, and enabling new market entrants. In this environment, mid-market companies’ ability to achieve growth will be challenging, due to the complexity in substituting what the market currently sees as standardised software features with new agentic offerings.

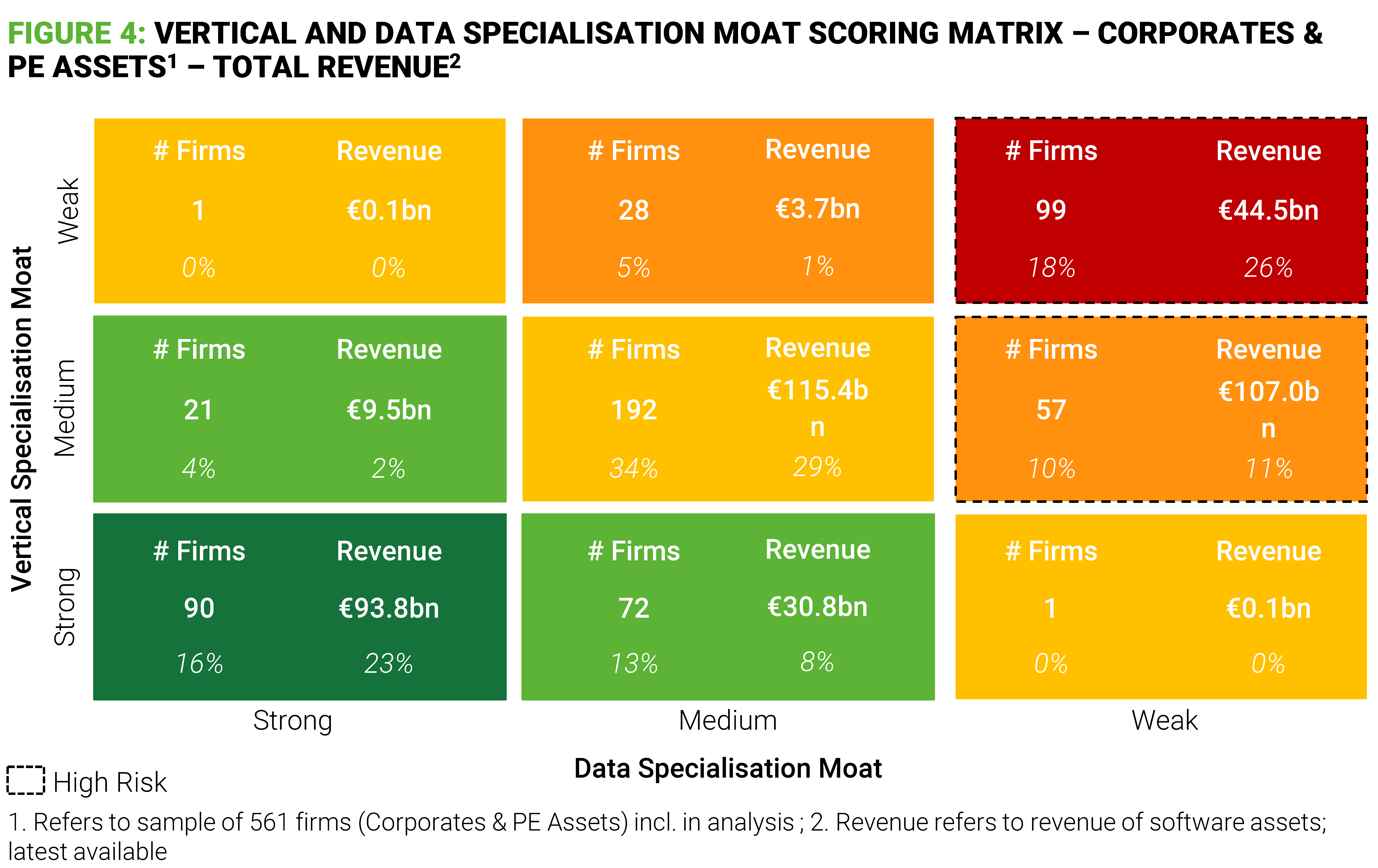

Moat evaluation – EMEA software sector

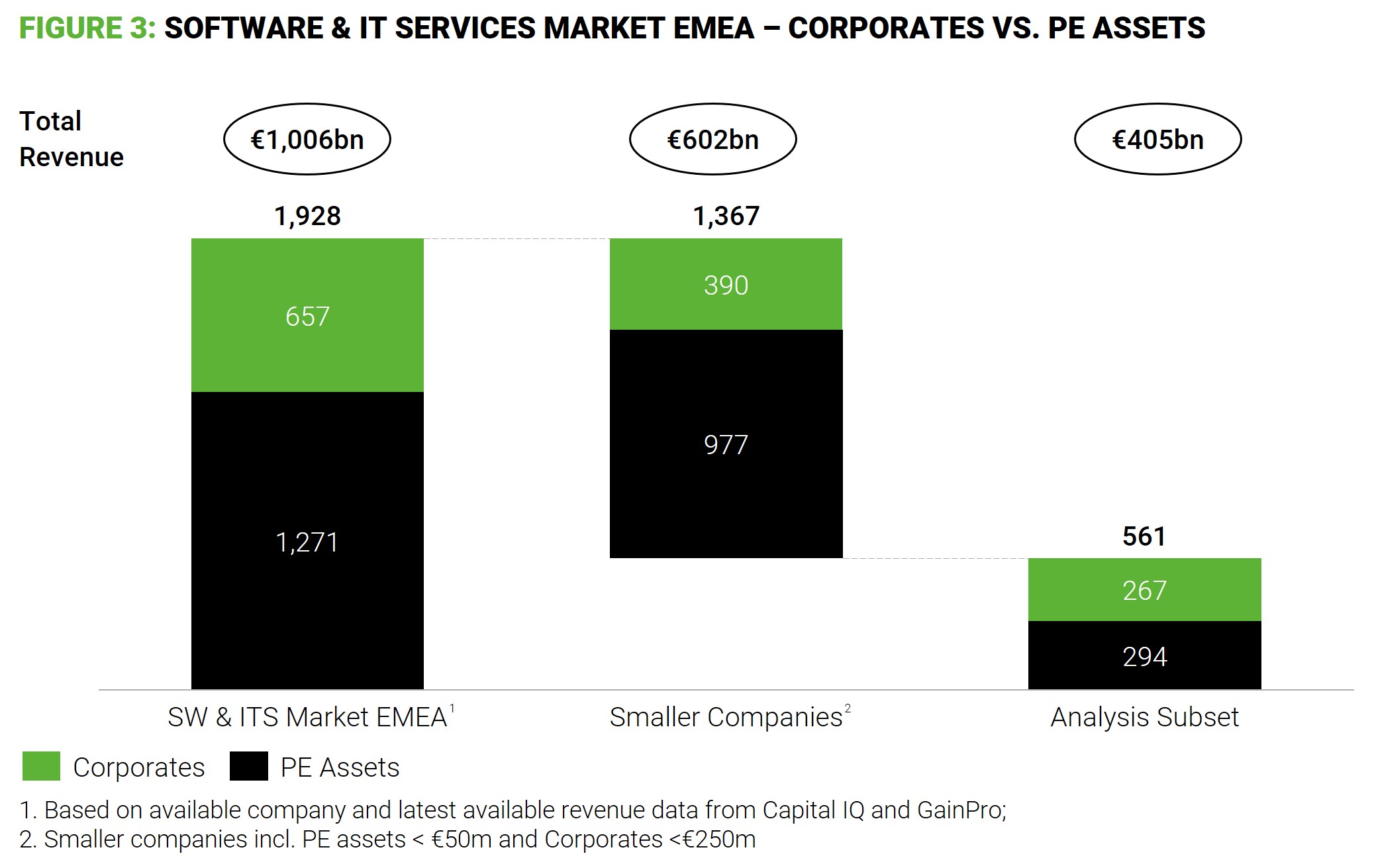

A “moat” is a characteristic that gives a software company a sustained competitive advantage. To understand where AI disruption will bite hardest, AlixPartners analysed the EMEA software and IT Services market – more than €1 trillion in revenues across c.2,000 companies – focusing on the 561 larger players that generate c.€405bn.

The dominant moats include:

We then scored each company for near-term disruption risk by combining an industry risk weighting with adjustments for each of the seven moats. Figure 4 shows the result: c.18% of firms – representing c.€44.5bn of combined revenues – are at high risk of AI disruption, driven primarily by weak vertical and data moats.

Key takeaways

We anticipate a split between resilient, AI‑enabled platforms and a longer tail of vendors facing mounting structural pressure.

Providers with strong and defensible moats – for example, those built on proprietary datasets, deeply embedded workflows or genuine ecosystem leverage – are better placed to pivot to outcome-based pricing and meet evolving customer expectations.

On the other hand, companies built around seat-based pricing, narrow feature sets, or commoditised data could struggle. Many are already encountering rising churn, slower new-logo acquisition, and heightened pricing pressure as AI agents replace or compress previously human‑centred workflows.

For PE sponsors, investors, lenders, and other financial stakeholders, a few key priorities emerge.

First, recognise that historic resilience is no longer a guarantee of success and that weak moats will be quickly exposed in the next refinancing cycle.

Second, re-evaluate key diligence metrics. ARR (Annual Recurring Revenue) may no longer be a reliable indicator of future performance (see our recent article, Rethink, retool, reprice: An agenda for software in the AI era). Diligence should also focus on data assets, workflow embedding, and AI readiness.

Third, look at businesses that are moving early on their transformation. Pricing model redesign, product consolidation, modernisation of tech stacks, and AI‑enabled efficiency levers will be essential to preserving value in mid‑market platforms.

While traditional SaaS playbooks are clearly no longer sufficient, understanding what it takes to adapt – and acting on this information – will define the winners and losers in the years ahead.