People

Jeff Goldstein

Partner & Managing Director, Americas Leader, Technology, Media, and Telecommunications

Boston

In 2026, we predict increased cooperation and consolidation between streamers and broadcasters. Dozens will announce new deals as they team up, exchange content, and embrace their competition as “frenemies” to win new customers and boost revenue.

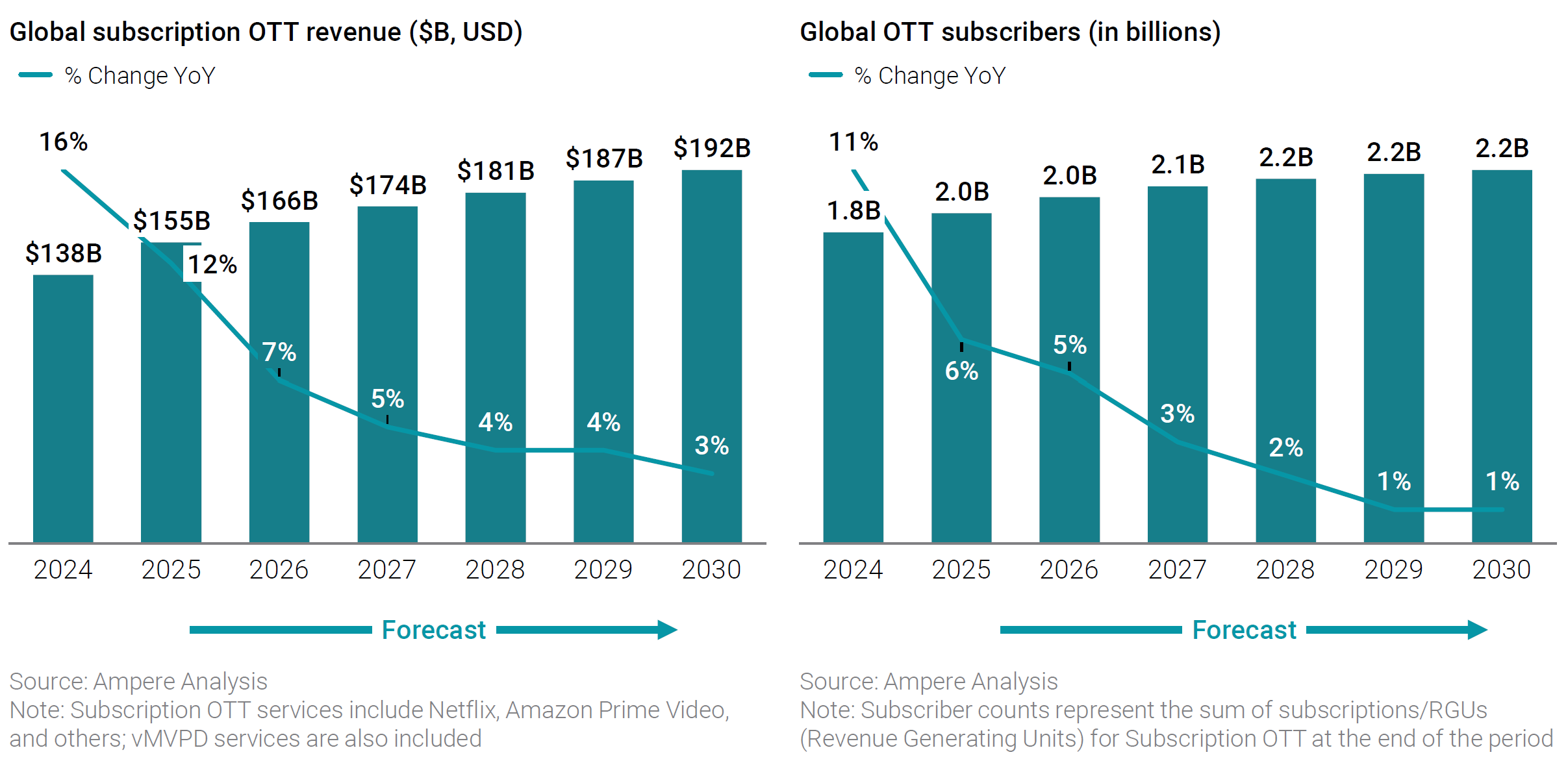

For the third year in a row, we begin our annual Media & Entertainment Industry Predictions Report by diving into the streaming wars. What began as a race for subscribers has evolved into a multifaceted battle for viewer attention and engagement. The global subscription over-the-top (OTT) market will surpass $165 billion in 2026, per Ampere Analysis. But with roughly 130 streaming companies chasing the same foundational value levers, there's only so much to go around—especially when the top five platforms (Netflix, Disney+ with Hulu and ESPN+, Amazon Prime Video, YouTube TV, and HBO Max) combine to generate nearly two thirds of current global subscription revenues.

The streaming industry is entering a mature phase, with global OTT growth expected to slow to 5% in 2026 and under 2% by 2030. Platforms like Netflix and Disney+ now focus on profitability, engagement, and average revenue per member rather than subscriber growth. Hybrid ad–subscription models have expanded reach but not consistent profits. To attract advertisers, streamers are investing in broad-appeal genres like live sports and procedurals, reflecting a shift toward scalable, advertiser-friendly programming.

OTT revenue and subscription growth are projected to slow

As content and ad-supported models collide, 2026 will bring fiercer competition and major consolidation. Deals such as RTL’s Sky Deutschland acquisition and Disney’s Hulu integration show how streamers are cutting duplication and costs. By sharing content, tech, and distribution, streamers aim to reduce churn and customer acquisition costs, signaling a new phase of strategic cooperation among rivals.

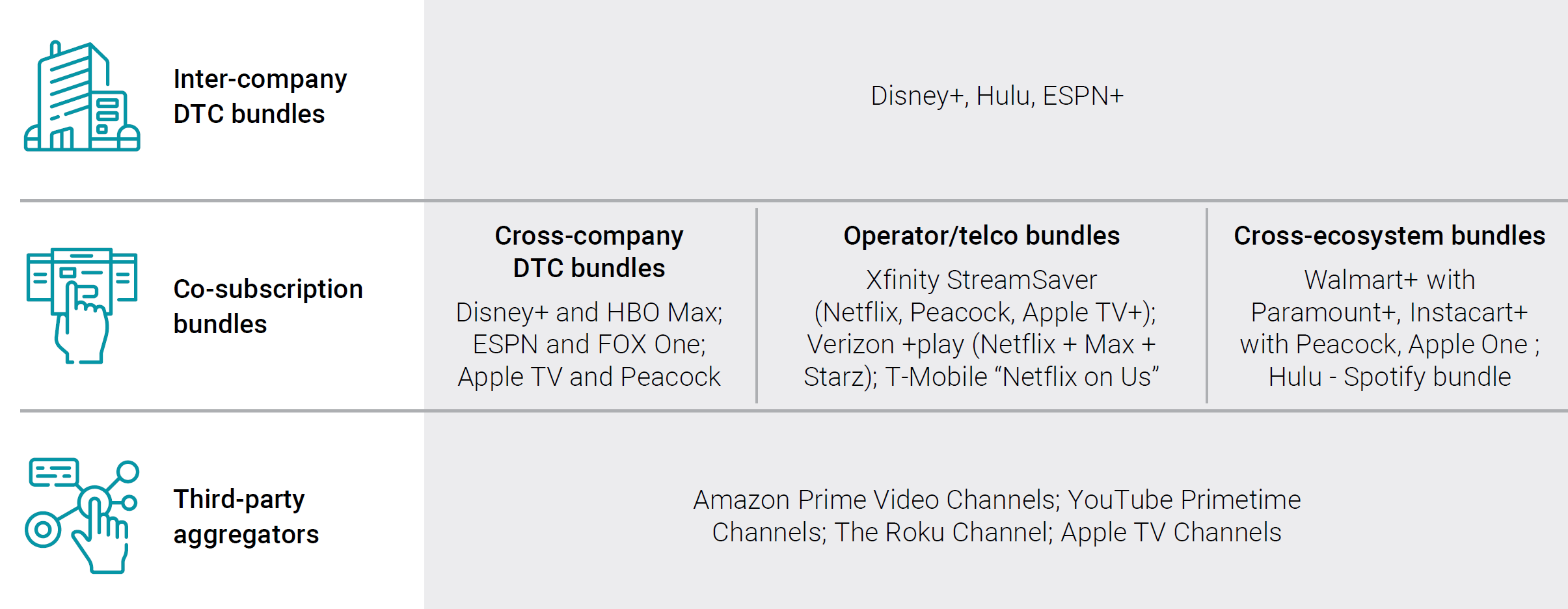

In the U.S., cooperation centers on DTC bundles and third-party aggregators. Telcos and retailers are bundling competing services like Netflix and HBO Max, while platforms such as Amazon Channels and YouTube Primetime integrate multiple SVODs into single ecosystems. Amazon takes around 30% of subscription revenue, but offers vast reach—one in three new U.S. streaming subscriptions originates via aggregators. Despite this, YouTube, Netflix, Disney, and Amazon dominate viewing time, while mid-tier players may consolidate or partner to stay competitive in 2026. We predict that two of these mid-tier platforms will either consolidate or establish deeper distribution partnerships to challenge the leading platforms and reshape the streaming hierarchy next year.

Streaming distribution ecosystem

Levels of cooperation vary by scale and strategy. Netflix and Disney maintain tight control over customer relationships, forming selective partnerships (e.g., telecom billing deals or Disney’s internal bundles) while avoiding deep integration with aggregators. Mid-tier players like Paramount+ and Peacock rely more heavily on bundling and wholesale deals with platforms like Prime Video to minimize acquisition costs. The emerging success factor is agility—knowing when to compete independently and when to cooperate for reach and cost efficiency.

Sports have become the ultimate test of cooperation. With U.S. sports rights surpassing $30 billion annually and split among multiple players, fragmentation has forced unlikely alliances. ESPN and FOX’s 2026 joint bundle exemplifies this shift, offering combined access at a discounted rate. As audiences seek simpler access to live content, “frenemy” collaborations are becoming the norm. Streamers now recognize that pooling sports assets drives engagement, retention, and profitability more effectively than competition alone.

In EMEA, a wave of collaboration between streamers and public broadcasters is reshaping the landscape. Partnerships such as Disney+ with ITV, Netflix with TF1, and Amazon with France TV are blending linear and digital ecosystems. These deals expand reach and diversify audiences—Disney+ gains older demographics, ITV gains younger ones, and French broadcasters gain access to large streaming bases. Netflix’s TF1 integration, in particular, signals a major strategic shift toward live linear content and third-party aggregation, potentially replicable across other European markets.

To win in a saturated market, streamers must innovate around bundling, discoverability, and live engagement. Investments in AI-driven personalization, UX, and interactive formats will define competitive advantage. AlixPartners expects three to five “central hubs”—YouTube, Netflix, Disney (with ESPN), and Amazon—to dominate distribution. Amazon is positioned to lead in aggregation, while YouTube and Netflix will battle for top share in viewership and revenue. The next phase of the streaming wars will reward adaptability, partnership, and consumer-centric design.

The media and entertainment world is shifting faster than ever—from streaming platforms merging short-form, long-form, and live content, to AI upending search and gaming, and M&A activity reshaping the landscape. Our annual Predictions Report dives into these trends, exploring who’s leading the charge, what’s next, and how businesses can stay ahead in a market defined by change. Click through to see where the industry is headed—and where opportunity lies.