Karsten Lafrenz

Partner & Managing Director - Zurich

“If the world were to end, I would want to be in Switzerland. Everything happens a little later there.” – Albert Einstein

The data from this year’s AlixPartners Disruption Index suggests that Einstein’s observation should be challenged by Swiss companies. In 2026, disruption has ceased to be a temporary shock to be weathered; it has become the fundamental operating climate of Swiss business. The historic “Swiss Finish”, once synonymous with stability and engineering excellence, must now be redefined around adaptability and resilience.

In a fragmented world defined by geopolitical volatility, regulatory flux, and environmental constraints, adaptability, not perfection, has become the foundation of durable competitive advantage. The time for radical adaptability is now, as our systematic analysis of the most recently published annual company reports and performance of all Swiss stock exchange (SIX) listed firms reveals.

Our analysis underscores that companies that acknowledge disruption and embed it into strategic planning outperform their peers. This “awareness premium” reflects the reality that recognition enables faster pivots, better investment choices, and more resilient business models.

Switzerland maintains its status as a premier global business hub, characterized by a highly educated workforce, economic stability, and a strong focus on high-value services and advanced manufacturing. The Swiss stock exchange reflects this diverse economy, hosting multinational heavyweights alongside dynamic mid-cap leaders.

Despite this relative stability, the 2026 AlixPartners Disruption Index confirms what has been observed since this study began: disruption is the new economic driver. Companies are moving through a “poly-crisis” era defined by rapid digitization, shifting customer behavior, fragmented geopolitics, and mounting economic uncertainty. Switzerland remains solid compared to its European peers. While the overall Disruption Score declined across Europe (72 to 67 points), Switzerland saw the sharpest drop (76 to 68 points), reflecting particularly turbulent years. Agility and technological integration are emerging as the new foundations of resilience.

Looking at the recent Swiss company reports data, major disruption themes can be observed and prove the AlixPartners Disruption Index findings:

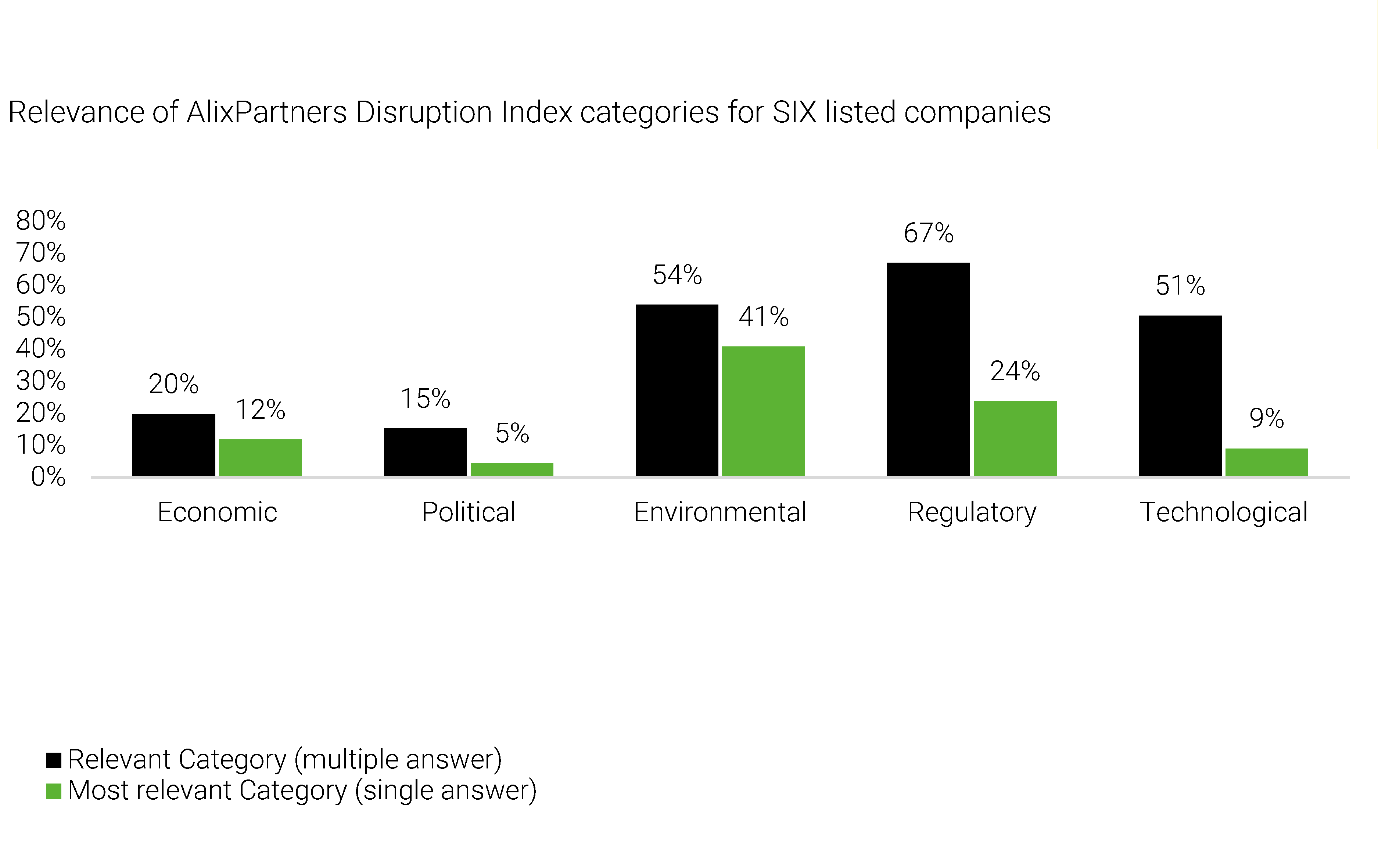

Relevance of disruption categories identified by AlixPartners' global Disruption Index

Disruption has become a systemic condition for Swiss companies rather than an occasional event. Analyzing the annual reports and performance of SIX listed companies based on categories from the AlixPartners Disruption Index framework, regulatory disruption appears the most ubiquitous category, with 67% of companies (up from 59% in previous year) recognizing it as relevant, and 24% identifying it as their most critical disruption category (same as 24% in previous year). The rising complexity of compliance, spanning data privacy, ESG reporting, and sector-specific governance, is likely driving this prominence.

Environmental and technological disruption follow closely. Environmental disruption remains central to corporate risk agendas, cited by 54% of companies (versus 46% in previous year). Sustainability is increasingly treated as a material disruption risk impacting supply chains, resilience, and reporting obligations rather than as a reputational matter.

Technology, however, is seldom a standalone issue; rather, it functions as a force multiplier, heightening competitive pressures and driving organizations toward capital-intensive transformation strategies. Client expectations have shifted markedly away from traditional advisory models and toward integrated, data-driven solutions that deliver speed, scalability, and measurable outcomes. This dynamic is clearly reflected in the data: while only 9% of annual reports identify technology as the single most important category (compared to 11% in the previous year), 51% reference it as one of several important factors (up from 42% last year), underscoring its broad and growing relevance across the corporate landscape.

Economic and Political disruption categories also warrant attention. Economic disruption, though less frequently mentioned, creates systemic uncertainty through volatility in interest rates and demand. Political disruption appears understated, likely because the annual reports were published before “liberation day” in April 2025, which significantly elevated the topic.

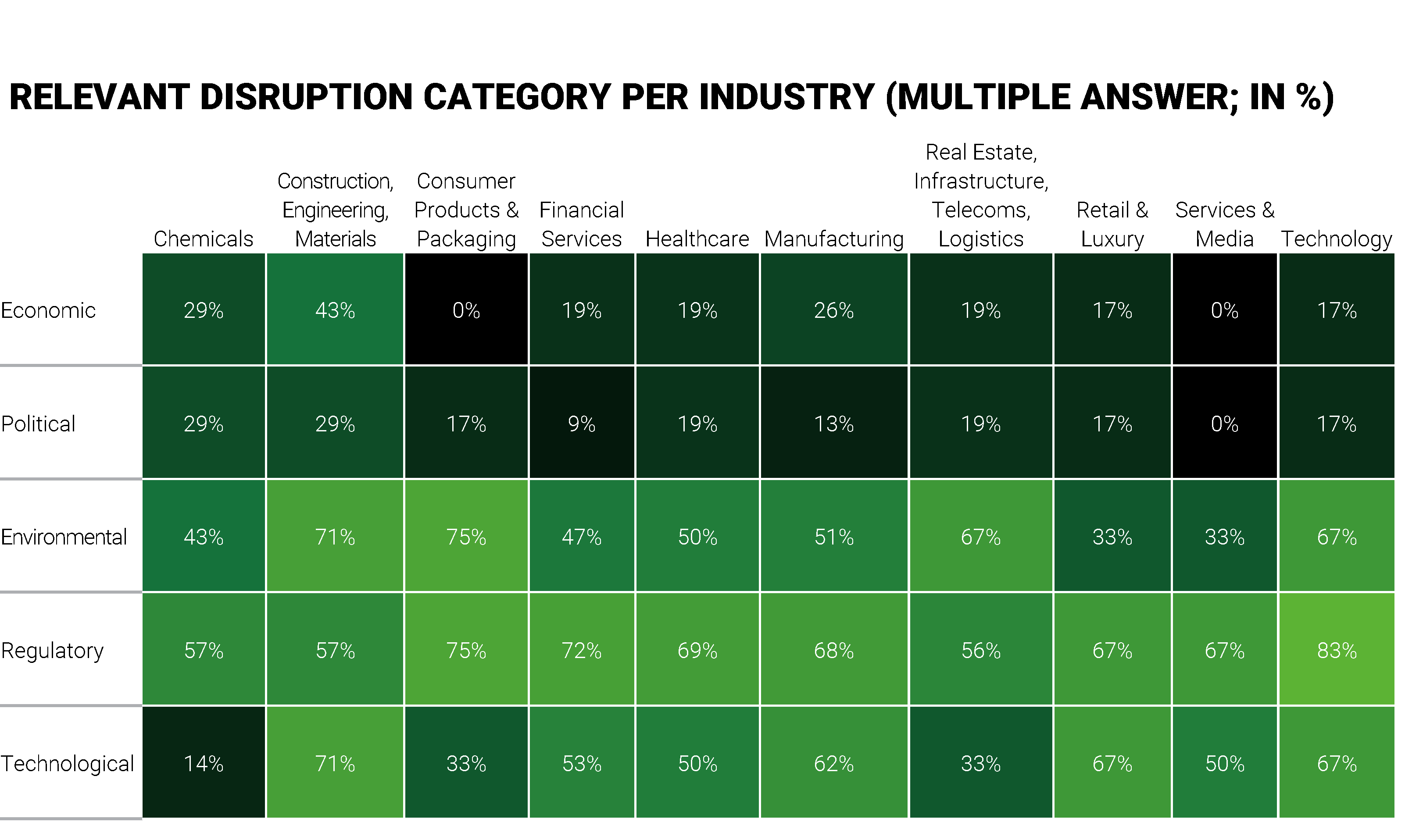

Disruption categories vary markedly across sectors. Regulatory disruption remains the only category relevant to more than 50% of companies in every sector. Other categories show pronounced sectoral variation.

Environmental disruption is especially important in resource-intensive industries such as Real Estate and Infrastructure, where carbon, energy, and resource constraints materially impact business viability. However, its cross-sector prevalence signals that environmental disruption has become a systemic challenge.

Technological disruption manifests differently across industries:

Competitive advantage is increasingly dependent on technological integration, not traditional differentiators.

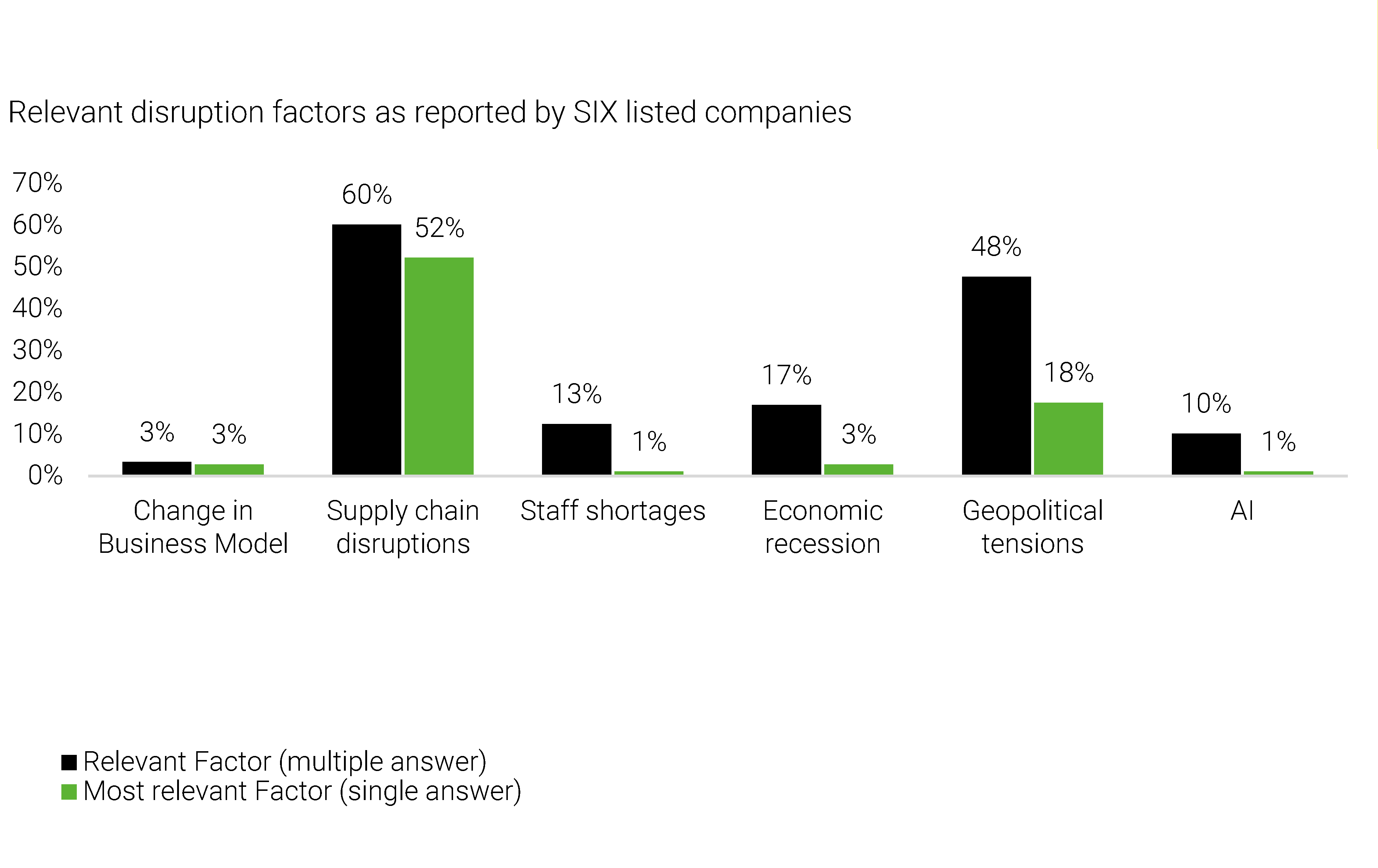

Disruption factors as reported by Swiss companies

When companies are analyzed for the individual disruption category reported in annual reports, the analysis shows that supply chain disruption is the most prevalent factor, cited by 60% of companies (same as 60% last year) and ranked the single most important factor by every second company (slightly up from 51%). The reasons are structural and pronounced. Switzerland is a hyper-globalized economy with a high foreign trade ratio. Unlike larger economies with domestic buffers, Swiss industry champions (e.g., Pharma, Machinery) operate as specialized nodes in complex global value chains.

Moreover, Swiss exports are typically low-volume but extremely high-value, making "just-in-case" strategies extraordinarily expensive. Capital tied up in inventories imposes a disproportionate burden compared to companies selling commoditized goods.

With 48% relevance, geopolitical tension is the next most cited factor, though slightly reduced from 57% last year. Geopolitics has evolved from a macro-risk into an operational threat that erodes historic Swiss advantages.

With increased pressure to comply with EU and US sanction regimes, Swiss companies also face higher regulatory burdens.

Geopolitics also impacts currency volatility. In periods of global uncertainty, capital flight to the Swiss Franc strengthens the currency and inflates export prices, weakening competitiveness.

Other factors, including imminent business model change, staff shortages, expected recession, and AI, follow at a considerable gap.

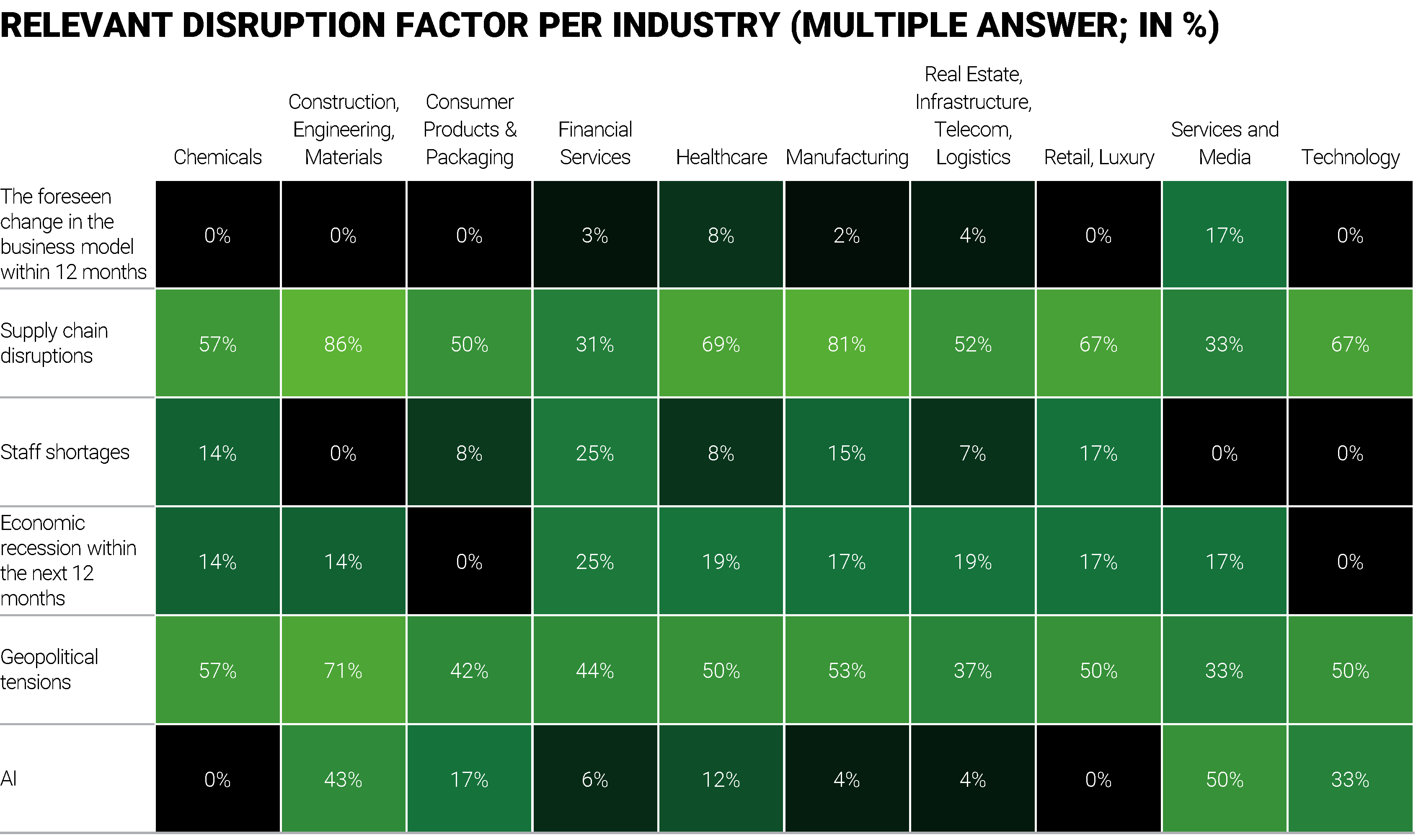

While supply chain and geopolitics are a shared burden, the other disruption factors are asymmetric across the industries. The foreseen change in business model is especially relevant for media & services companies. Particularly media companies continue to face competition from international technology giants for advertising spend, rapidly evolving consumer tastes in the digital age, and a highly dynamic content landscape.

Staff shortages and economic recession are especially relevant for financial services companies. Modern banks are desperate for a hybrid profile: professionals who understand complex Swiss compliance regulation and possess advanced data science/AI skills. This combination leaves critical strategic roles vacant. While an economic recession hurts every sector, the financial industry is the "gearbox" of the economy. When the economy slows, the impact on finance is magnified through multiple channels.

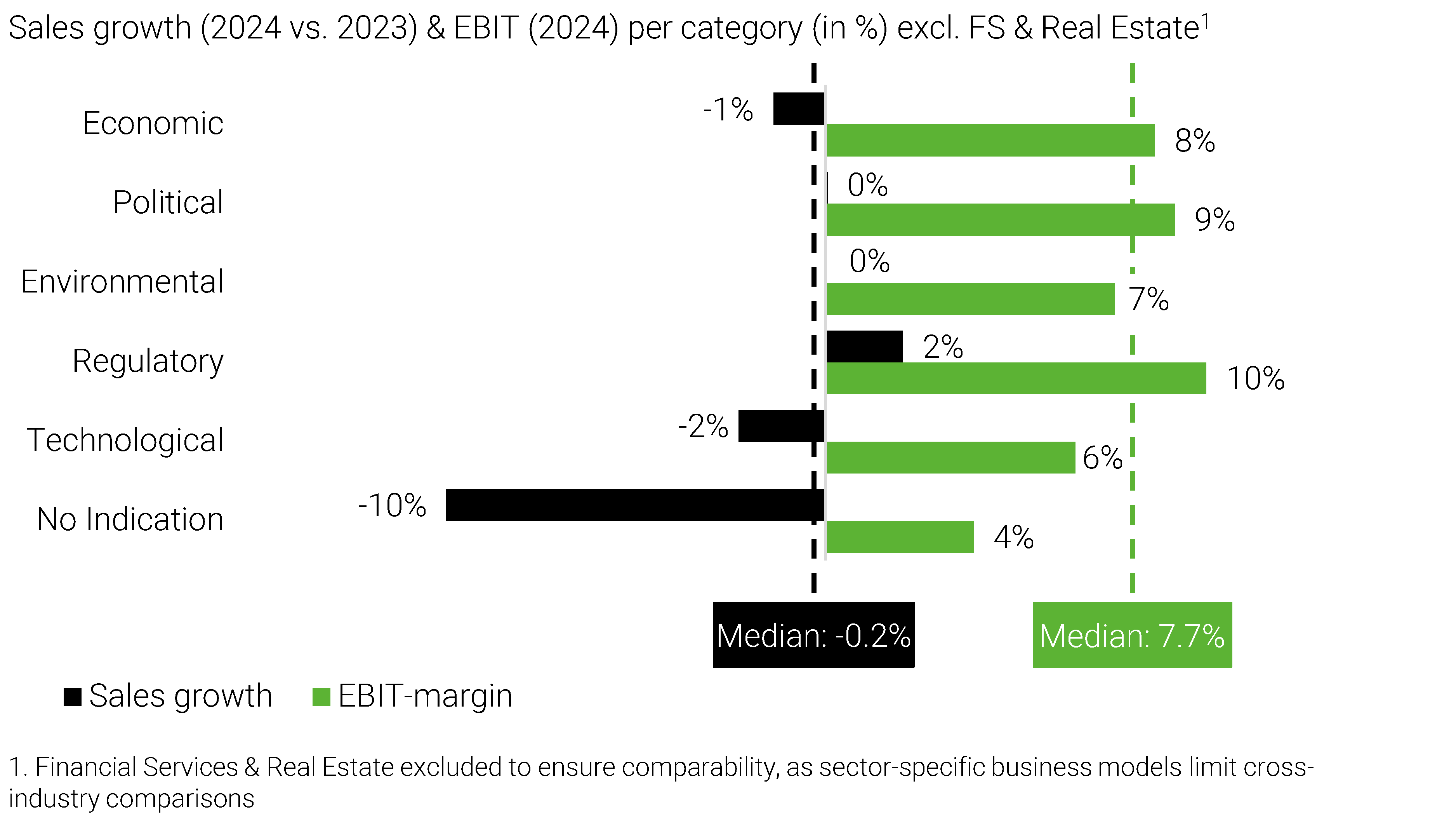

A central finding of the study is the performance divergence between companies that acknowledge and actively manage disruption and those that display “no indication” of disruption in their disclosures.

Data points to an “awareness premium” in performance: companies that explicitly identify – and hence manage – disruption, such as political or economic disruption, demonstrate stronger resilience in EBIT margins and revenue growth when compared to firms in the “No Indication” group. The latter cohort exhibits lower strategic agility and is more prone to reactive rather than proactive responses, suggesting that under-recognition of disruption may be a leading indicator of underperformance.

This analysis, split into eight industry deep dives, analyses disruption patterns across companies listed on the SIX Swiss Exchange, covering major sectors of the Swiss economy including manufacturing, financial services, healthcare, real estate, and consumer products – sectors in which AlixPartners’ experts operate globally and within Switzerland. The analysis uses artificial intelligence to systematically process the most recently available annual reports from publicly listed Swiss enterprises and identify categories and drivers of disruption that shape business performance and competitive positioning.

The research employs a dual analytical framework combining deductive and inductive research methodologies. The analysis offers a comprehensive view of disruption intensity, prevalence, and performance impact across listed Swiss companies, providing strategic insight for investors, executives, and stakeholders navigating an increasingly dynamic landscape.

More articles of this series: