Karsten Lafrenz

Partner & Managing Director - Zurich

Switzerland's Consumer Products & Retail sectors encompass a diverse range of businesses from product manufacturing and packaging through traditional mass market retail to high-end luxury goods and watchmaking. The industries benefit from Switzerland's global reputation for quality, precision and premium position in global markets. However, they face profound structural challenges from changing consumer behaviors, new technologies, as well as environmental and regulatory pressures. Economic headwinds dampen consumer sentiment and lower discretionary spend in many of the Consumer Products & Retail segments, as companies struggle with productivity constraints and the need for substantial business model transformation.

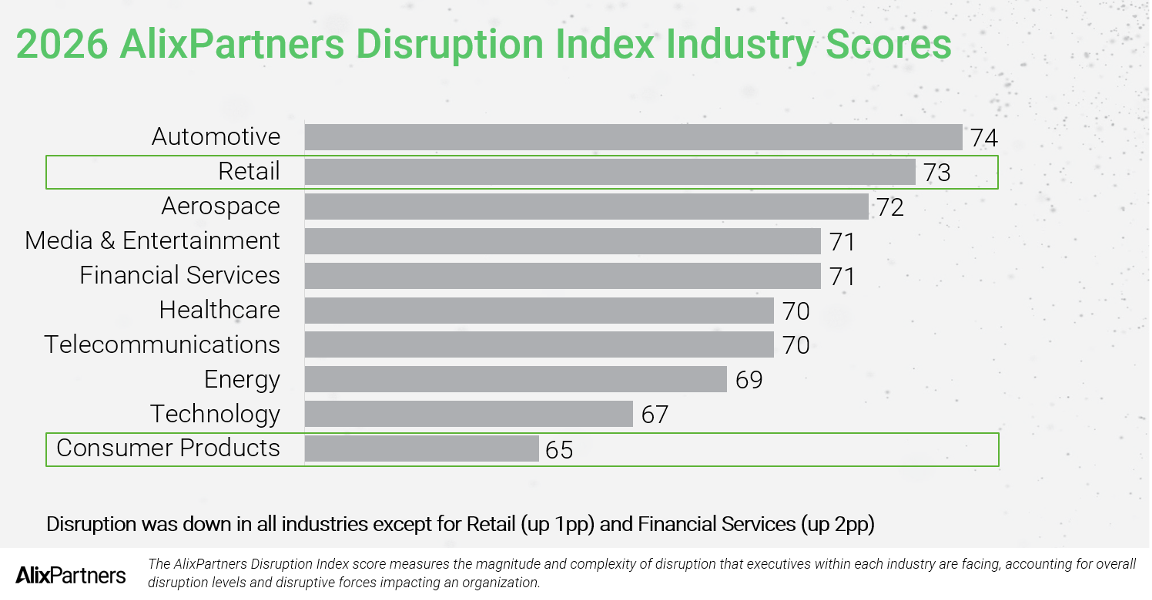

According to the 2026 AlixPartners Disruption Index, the Retail industry continues to face very high levels of disruption, while the Consumer Products industry faces more moderate levels.

The industries' fundamental challenges become visible in the following systematic analysis of the most recently published annual company reports and performance of Swiss stock exchange (SIX) listed firms.

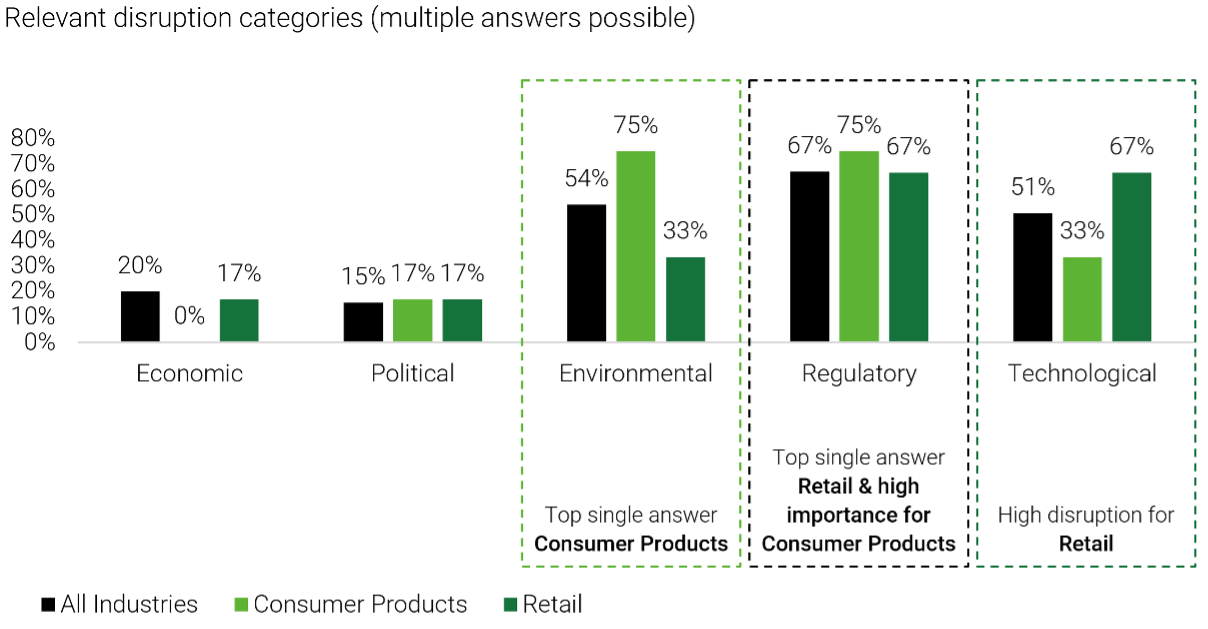

Key disruption categories based on AlixPartners’ Disruption Index

Based on categories from the AlixPartners Disruption Index framework, the two industries are not being impacted by disruption the same way. While Consumer Products shows highest disruption in Environmental and Regulatory, Retail shows highest disruption in Technological and Regulatory categories, with Environmental a close third category. This mirrors the expectations consumers, employees and business partners bring: environmental disruption captures rising demands for sustainability, concerns over waste, and calls for greater transparency across supply chains.

Retail companies face more pressure from technological disruption reflecting the e-commerce transformation, omnichannel requirements, digital marketing, and AI-powered personalization that fundamentally reshape classical retail models and D2C channels. Regulatory pressures affect both industries strongly and similarly, stemming from consumer protection laws, data privacy requirements and sustainability regulations, among others.

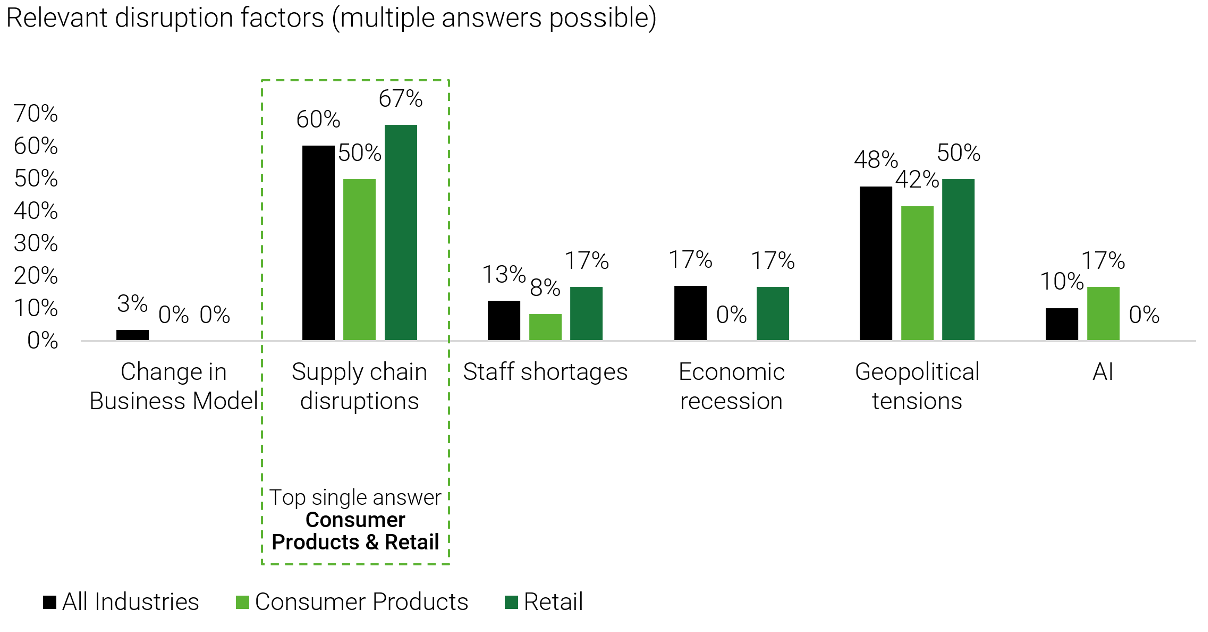

Key disruption factors as reported by Swiss companies

Supply chain disruptions affect retail and consumer companies as the most important factor by far, reflecting complex global supply chains exposed to availability, accessibility, and affordability issues.

Geopolitical tensions impact as the second most important factor through international trade and tourism, cross-border shopping patterns, and supply chain dependencies. Most recently, tariffs in important markets such as the US have added another layer of complexity and insecurity across both sectors.

Staff shortages rank #3 in Retail, while AI ranks #3 in Consumer Products. Retail's bottleneck remains largely physical, associated with store associates, warehouse staff, transportation staff and other roles which command less demand. Consumer Products companies, less exposed to frontline headcount, are further along in confronting AI as a structural force reshaping the business model including product development, marketing spend, and the route-to-consumer. Looking ahead, AI's role as a disruptive force is only set to grow across both sectors.

The Consumer Products and Retail companies analyzed demonstrate stagnating revenues and below‑median EBIT margins relative to the cross‑industry sample, which is not uncommon for these notoriously low-margin industries.

The performance of the individual Retail and Consumer Products firms varies, however, depending on the disruption categories they identify in their annual reports. Companies within the sample that explicitly disclose environmental disruption in their annual reports show higher average EBIT margin than peers that do not. Consistent with broader cross-industry tendencies, the findings suggest that active identification of disruption, particularly environmental and regulatory, correlates with more stable profitability, even if it does not fully offset growth pressures inherent to the sectors. Conversely, lack of disclosed disruption awareness correlates with weaker growth outcomes, supporting the interpretation that strategic anticipation and transparency act as proxies for preparedness.

Companies embracing disruption unlock substantial value creation potential. With respect to the disruption categories highlighted above, this translates into opportunities:

The disruption factors point to equally concrete opportunities:

In light of persistent macroeconomic turbulence and consumption headwinds, Retail and Consumer Products companies may struggle to sustain past performance levels. Traditional retail companies may continue facing structural decline in foot traffic, margin pressure, and business model challenges as e-commerce penetration grows, requiring ongoing investment in digital capabilities. Consumer companies, meanwhile, will face stronger regulatory pressure and expanding sustainability disclosure requirements.

For both Retail and Consumer Products companies, cost management will be critical.

Yet there is more to it. After several rounds of cost-cutting, the obvious levers are exhausted in most companies. The next wave of savings won't come from doing the same things cheaper. It must come from a critical reassessment of the operating model itself to initiate genuine structural transformation.

We expect many Consumer Products and Retail companies to adopt a restructuring mindset, rethinking their strategy, structure and execution fundamentally. This means moving beyond incremental tweaks to embrace bold, transformative changes and regain momentum across three areas for action:

In both sectors, the companies that move first and anticipate disruption will reap the greatest rewards from their transformation.