Jason McDannold

Americas Co-Lead, Private Equity, Partner & Managing Director

Chicago

Jason McDannold

Partner & Managing Director - Chicago

AI’s overhaul of the tech industry will leave no stone unturned, and the AdTech sector is feeling the effects. AI, connected TV (CTV), and privacy-safe open-web buying are now table stakes, not differentiators. But as they converge within the advertising ecosystem, not every company is utilizing these tools to drive actual value.

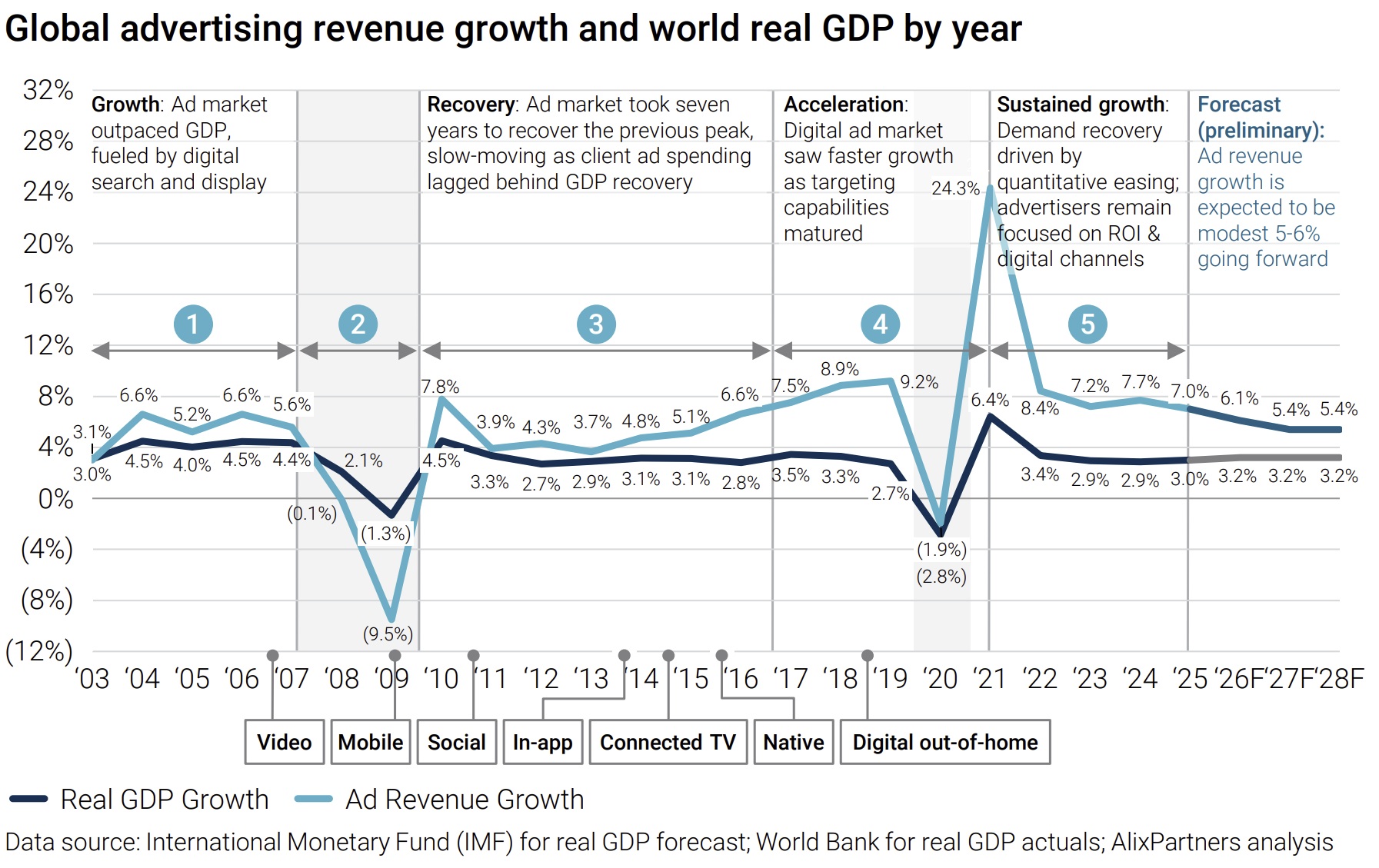

According to our analysis, nearly one in three U.S. digital ad dollars will go to CTV and premium online video this year, an increase from 27% in 2025 (per IAB). Digital spend is still growing, but incremental dollars are flowing to platforms that prove outcomes and simplify buying, not just those with the most connected surfaces. It’s about doing less and going deeper—hyper-targeting media spend towards where buyers are investing and strategically leveraging those channels to maximize margins. As the economy faces continued pressure and limited growth, advertising spend is not expected to increase significantly in the near term. Instead, ad spend is likely to remain closely correlated with GDP growth trends.

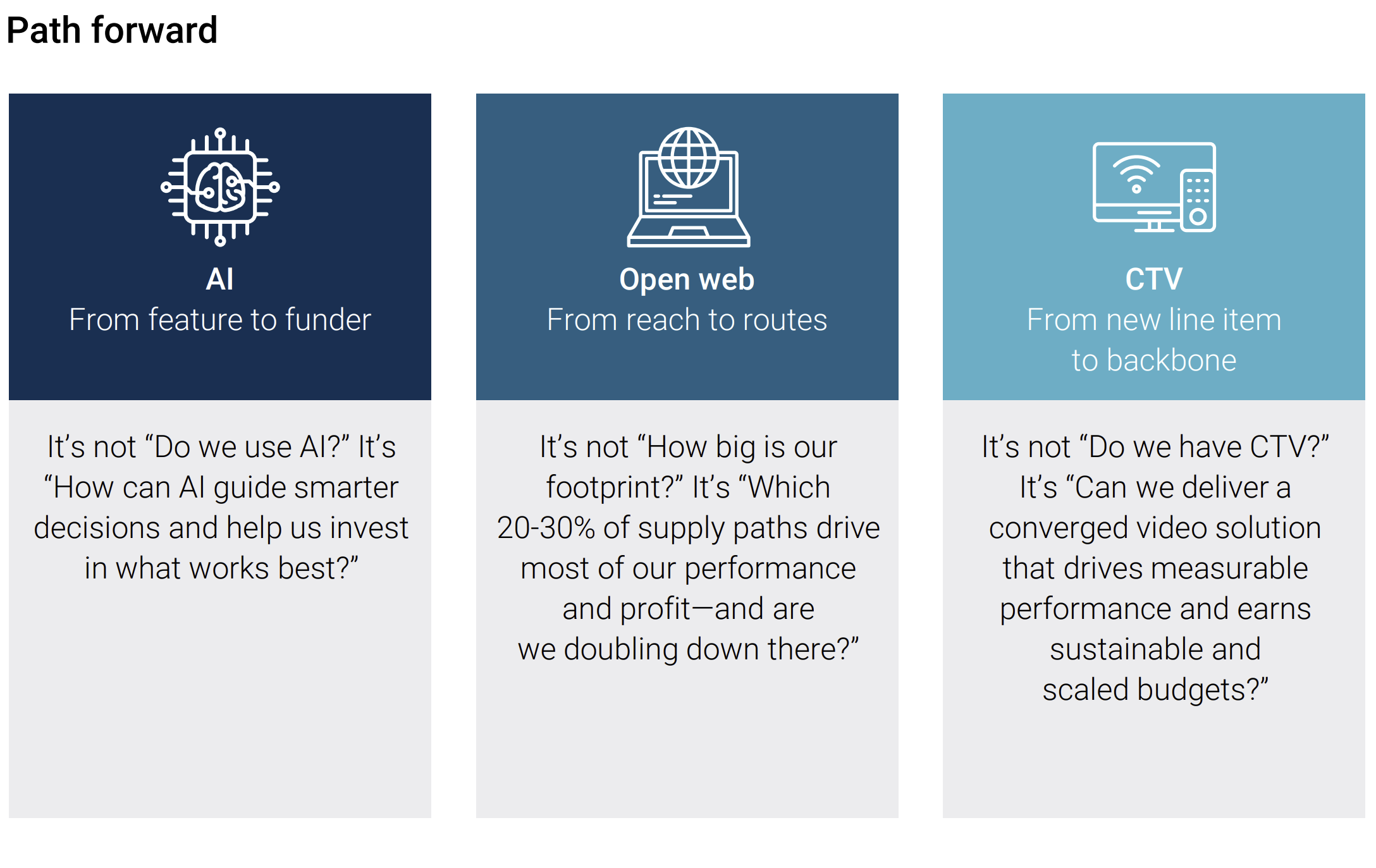

The real separation in 2026 and beyond could come down to three shifts, not three new trends:

AI is shifting from a tool that optimizes ads and ad placements to becoming the core engine for ad planning, targeting, and measurement across the digital landscape (search, social, open web, CTV, retail media, and more). Agentic AI allows companies to micro-segment via ongoing behavioral analysis and optimize channel strategy by assessing real-time performance.

Open web is shifting from an emphasis on impressions, views, and reach (seen more as vanity metrics) to fewer but higher quality placements that target granular customer segments.

CTV is shifting from another channel to the default TV/video line item for advertisers, with sustained double-digit growth but heavy competition in a saturated market.

Previously, ad placements were largely automated. Companies chose websites and mobile screens with the right target audiences, paid for real estate, and software sorted out which ads went where.

But now, AI is redefining the process by which ads are created and placed. An airline could, hypothetically, see if a potential customer is asking ChatGPT about comfortable seats or environmental concerns, and tailor ads with custom messaging based on AI agent conversations.

While most platforms already use AI in bidding for ad space, in 2026 we’ll see a further shift whereby AI goes from an execution tool to the portfolio brain that oversees which audiences, channels, and ad tactics deserve dollars.

What’s working?

Using AI to score and prioritize segments, creative, and supply paths based on predicted business outcomes, not just clickthrough rate (CTR).

Running AI‑driven “keep / grow / kill” reviews on tactics and products to reallocate spend and R&D faster.

Selling named AI products—e.g., “Optimization Layer” or “Outcome Audiences”—with clear commercial impact and proof.

What’s not working?

Generic copilots and auto‑bidding without net revenue retention (NRR) or a margin story behind them.

Roadmaps and trading decisions that look the same as 2-3 years ago but with “AI” labels added.

Black‑box models buyers must take on faith.

Immediate priorities: Put AI in front of management

Decide three places where AI will explicitly change what you fund in 2026, not just how you buy.

Make 1–2 AI products commercially visible—with clear pricing, case studies, and proven lift—while leveraging AI to drive operational efficiency and effectiveness.

Selling at open-web scale is nothing new; buyers know they can buy trillions of impressions. But now, they are shifting from a focus on impressions and views and towards optimizing every dollar.

In 2026, advertisers will embrace more curated, high-quality, privacy-safe routes that protect ad performance and margins. When given the choice between spending the same amount of money for one million random views, or 100 views by ideal target customers, companies are choosing the latter.

What’s working?

Curation as a product: Move beyond bundling to curate the right mix of marketplaces that maximize ROI—anchored in quality, attention, and outcomes, not formats.

Privacy‑first by default: Clean rooms, first‑party IDs, and consented integrations baked into core offerings, not side projects.

Surfacing supply paths, quality scores, and economics in the user interface so traders can choose fewer, better pipes.

What’s not working?

Optimizing for scale and impressions over quality (such as chasing long‑tail inventory to hit volume targets which dilutes performance, transparency, and take rate).

Treating fraud/brand safety as a “check-the-box” item rather than performance levers tied to ROAS and margin.

Relying on opaque identity and supply paths that may work in the short term but lack transparency, durability, and regulatory defensibility.

Immediate priorities: Quality over quantity

Identify 3-5 curated/quality paths to grow and 3-5 legacy paths to actively wind down.

Report margin and performance by supply path to your own leadership as a first step.

Reallocate spend toward a focused set of high-performing, curated supply paths.

First advertisers fawned over the internet, social media, and mobile apps. Now their obsession is CTV.

The winners in this space are going a step further than simply integrating ads into the TV experience—they’re embedding content within experiences so seamlessly it doesn’t feel like an ad at all. In 2026, the major shift is from selling CTV as a channel to owning converged video planning and ad performance across CTV, online video, and even social media.

What’s working?

CTV + web video sold as one plan: Unified frequency, guardrails, and reporting where privacy rules allow.

CTV tied to commerce, retail media, and attention metrics so it competes with performance budgets, not just awareness.

Operational simplicity: Standardized deals and workflows so CTV doesn’t feel like a bespoke project every time.

What’s not working?

“We have CTV too” as another line item, with separate teams, budgets, and reports.

Selling raw streaming inventory without a reach, attention, sales story, or clear ROI.

Opaque reselling and daisy-chained paths that scare off sophisticated buyers.

Immediate priorities: Decide if you will be a video spine or a CTV add‑on

Define 1-2 converged video products that bundle CTV + web under a single outcome metric.

Commit to 1-2 tangible steps to simplify CTV buying (e.g., standard package, service-level agreement on launch times, one reporting view, real self-service capabilities) that make performance-focused CTV easier to transact and measure.

You already play in AI, open web, and CTV. The question for 2026 and the immediate future is where you choose to sharpen the edge—and how quickly you can demonstrate impact across your revenue mix, NRR, and margins.