Insights

2026 Home Delivery Survey

NEW YORK (June 23, 2026) -- AlixPartners, the global consulting firm, today released findings from its annual Home Delivery Survey of U.S. consumers and supply chain executives. According to the survey respondents, consumers now expect free delivery in under three days, 52% will boycott a retailer after just 1–2 botched deliveries, and 64% of executives say home delivery is not yet profitable. But AI is emerging as a critical lever for cost and customer experience.

AlixPartners’ 14th annual study of U.S. consumer expectations and executive strategies across the home delivery ecosystem revealed a sector under mounting pressure: delivery has become the decisive battleground for customer loyalty, yet the economics of fulfillment continue to deteriorate for most retailers.

The speed and free shipping imperative

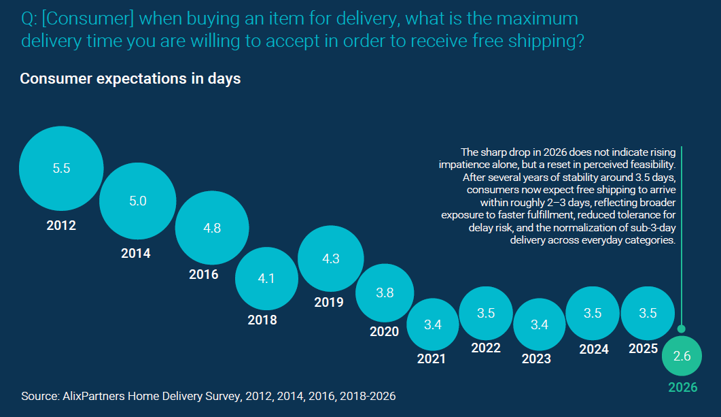

The most striking finding in this year's survey is the accelerating compression of consumer delivery expectations. Free shipping is now a near-universal demand. 94% of consumers say free shipping impacts their purchase decisions, with nearly 70% saying it has a 'great impact.' Two in three shoppers abandon their cart entirely when shipping fees exceed approximately $10, and more than 25% expect $0 shipping as a baseline.

Speed expectations have tightened in parallel. Consumers now expect free delivery in an average of 2.7 days — down from 3.5+ days in prior years — with expectations varying sharply by category, from 0.9 days for grocery and food to 3.2 days for large general merchandise. More than 20% of demand is estimated to be at risk when these timing expectations are not met.

“The speed and free shipping expectations consumers hold today were once reserved for Amazon Prime members. They are now the floor — not the ceiling — for every category of retail,” said Marc Iampieri, Global Co-Leader of Logistics & Transportation and Partner & Managing Director at AlixPartners. “Retailers who treat home delivery as a cost line to minimize, rather than a customer experience to invest in, are quietly surrendering loyalty they may never recover.”

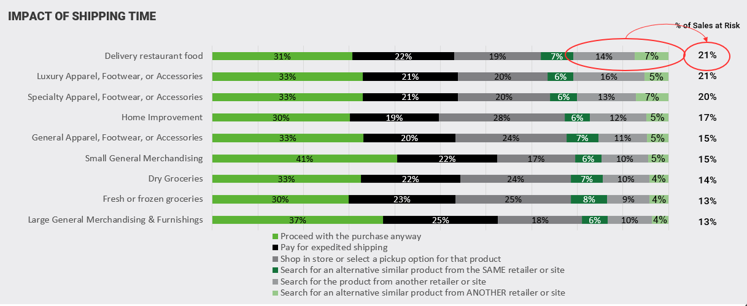

~20% of consumer respondents will shop elsewhere if minimum expectations for free shipping are not met, with delivery of restaurant food, apparel & footwear the highest at risk

Delivery failures are destroying loyalty — fast

The survey makes clear that a single bad delivery experience can permanently alter a customer relationship. More than 85% of consumers say a poor delivery experience reduces their willingness to repurchase from that retailer. Critically, an apology alone is not sufficient: nearly 90% of shoppers say a late delivery at least weakens — or ends — their relationship with the retailer, even when the retailer responds with an apology. Compensation, transparency, and a credible updated ETA are what consumers expect.

Repeat failures are even more damaging. More than half of consumers say they would boycott a retailer entirely after just 1–2 missed deliveries. And while consumers assign primary blame to the delivery carrier when things go wrong, it is the retailer who absorbs the commercial consequence.

“In fashion and apparel, the last mile is the last impression. When a package arrives late, damaged, or without communication, the brand takes the hit — not the carrier,” said Chris Considine, Partner in AlixPartners’ Retail practice. “Our clients in specialty retail and luxury are now treating carrier selection and delivery communication standards as core brand decisions, not operational afterthoughts.”

The economics of home delivery are under pressure

For retailers, the delivery imperative comes at a painful financial cost. According to the executive survey:

In response, retailers are reshaping fulfillment economics through a combination of spend thresholds, bundled membership programs, and behavioral nudges. The survey finds that more than 80% of consumers will accept slower delivery in exchange for incentives — a signal that 'no-rush' delivery options represent a significant, underutilized lever for margin improvement and operational smoothing.

“The grocery and consumables sector is facing a particularly acute version of this problem,” said Matt Hamory, Co-Leader of AlixPartners’ Global Grocery practice. “Consumers expect near-instant delivery for essentials, yet the unit economics of same-day fulfillment are extremely difficult to make work at scale. The winners will be those who can segment their customer base effectively — offering premium speed to those who will pay for it, while nudging the rest toward lower-cost options through smart incentive design.”

Carrier strategy: reliability has overtaken price

For the first time in the survey's history, reliability has displaced price as the primary criterion for selecting a lead carrier. The UPS-FedEx duopoly is meaningfully eroding: 55% of retailers now use carriers outside of UPS, FedEx, and USPS, and more than a third have actively shifted volume away from traditional incumbents in the past year. FedEx has overtaken UPS as the most-cited primary carrier, used by 38% of retailers, compared with UPS's 35% peak in 2023.

On the consumer side, Amazon leads all carriers in overall delivery preference — topping rankings for timeliness and condition of delivery — while USPS ranks lowest for both timeliness satisfaction and technology investment alignment. Notably, 84% of consumers say their past delivery experiences, including which carrier is used and whether the driver is a gig worker, directly influence where they choose to shop.

“Carrier diversification used to be a cost play. It is now a resilience and brand play,” added Considine. “The retailers gaining ground are those who have built multi-carrier architectures that let them route around service failures in real time — and who understand that for their premium customers, the carrier badge on the box is part of the product.”

AI emerges as the next competitive differentiator

Across both the consumer and executive surveys, artificial intelligence is emerging as a high-confidence investment priority in home delivery. Executives' top AI priorities include more reliable ETAs, reduced failed deliveries, and real-time routing optimization. These map directly with consumers' wish list, which is led by live tracking and 24/7 proactive delay notifications. This rare consumer-executive alignment creates a high-conviction investment signal.

AI adoption is already underway: address validation and AI-powered customer service bots lead current deployments. Over a 2 to 3-year horizon, executives are prioritizing ETA accuracy, routing optimization, and network capacity planning. On the consumer side, three in five shoppers report having used an AI chatbot for delivery tracking or issue resolution. Consumer comfort with AI throughout the shopping journey is broadly positive — particularly for product recommendations, delivery updates, and resolving service issues — provided the experience is fast and effective.

Returns: the hidden loyalty lever

Returns policy has become a front-door driver of conversion. Most shoppers review a retailer's return policy before completing an online purchase, and only approximately one in three say their return frequency would remain unchanged if charged for return shipping. Product quality issues and damaged goods remain the leading reasons for returns, with apparel and footwear generating the highest return volumes overall.

About the survey

The 2026 AlixPartners Home Delivery Survey has been conducted annually since 2012. The 2026 edition was fielded between April 28 and May 4, 2026. The consumer survey polled U.S. consumers aged 18 and older across all regions, demographics, and income levels. The executive survey polled senior professionals in transportation, logistics, and supply chain functions from North American companies with $100 million or more in revenue. Both surveys were conducted online and were re-weighted to reflect accurate demographic and firmographic distributions.

About AlixPartners

AlixPartners is a results-driven global consulting firm that specializes in helping businesses successfully address their most complex and critical challenges. Our clients include companies, corporate boards, law firms, investment banks, private equity firms, and others. Founded in 1981, AlixPartners is headquartered in New York and has offices in more than 20 countries around the world. For more information, visit www.alixpartners.com.

Media Contact:

Ed Canaday

[email protected]

+1 917-434-5075